Why should your family's home be the collateral for your company's growth? In the rapidly expanding corridor of Melbourne’s west, many local entrepreneurs are discovering that a business loan without property security Thornhill Park is no longer a distant dream but a practical financial tool. With the western suburbs leading the state in new business growth throughout 2025 and 2026, the traditional bank "no" is being replaced by flexible, asset-based solutions that prioritise your cash flow over your home's equity.

We know how exhausting it is to face endless paperwork only to be told your personal property must be on the line. You've worked hard to build your enterprise, and you deserve a path to capital that respects your personal boundaries. This guide explains how to secure the funding you need while retaining a clear title on your home, even if you're managing a new ABN or navigating contractor income. We'll preview the current 2026 lending landscape, including streamlined application processes and the latest interest rate trends, so you can grow your business with quiet confidence and total security.

Key Takeaways

- Understand why modern lenders now prioritise your business cash flow and performance over a mortgage on your family home.

- Discover how to secure a business loan without property security Thornhill Park by utilising the PPSR to protect your most valuable personal assets.

- Compare the specific tax benefits and costs of asset finance structures like chattel mortgages against general unsecured loans.

- Use our five-step preparation checklist to ensure your application is fast-tracked and your credit file is positioned for success.

- Learn how partnering with a specialist broker removes the heavy lifting from the application process, letting you stay focused on your trade.

The Property Trap: Why Thornhill Park Business Owners Are Seeking Alternatives

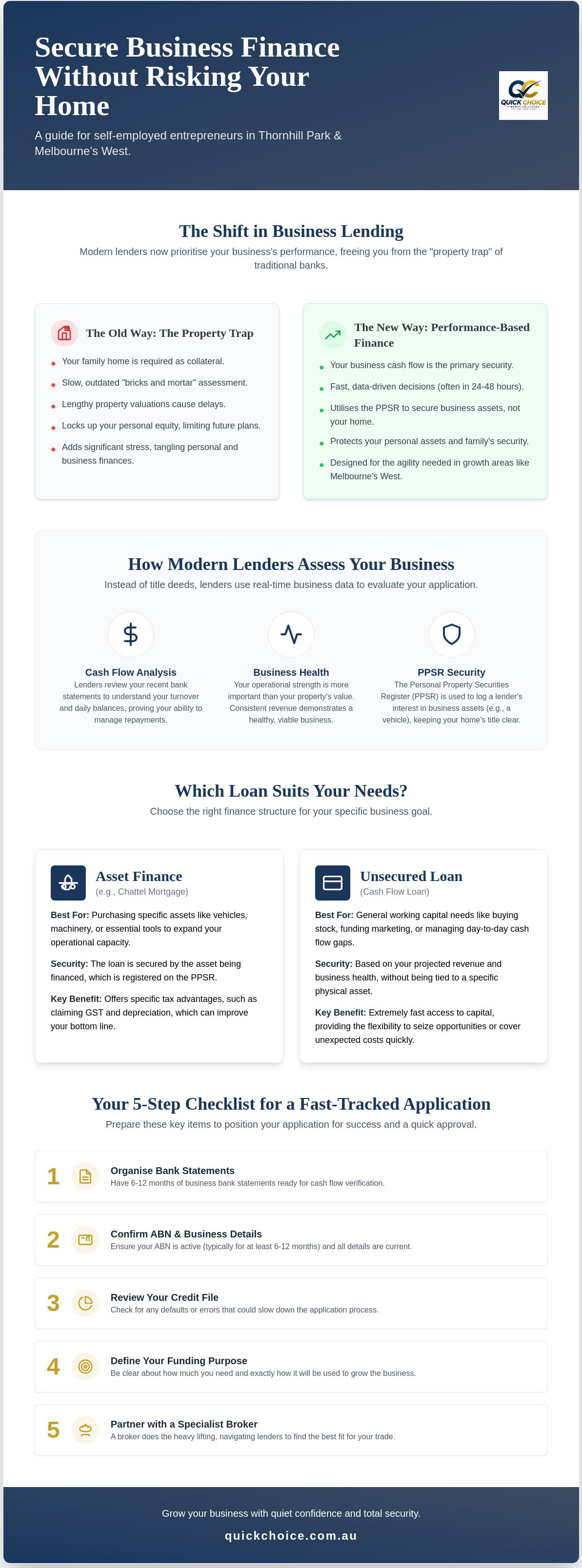

Traditional banks often operate on an outdated "bricks and mortar" mindset. They view your business potential through the lens of your home equity, which creates a significant barrier for many local entrepreneurs. A business loan without property security Thornhill Park is a specific type of finance where your residential or commercial real estate is never used as collateral. In 2026, this distinction is more important than ever. While major lenders might still demand a mortgage over your family home for a simple cash flow injection, modern lending focuses on your business's actual performance.

This type of finance is a strategic form of unsecured debt, where the lender evaluates your bank statements and turnover instead of your title deeds. It allows you to access capital based on the strength of your operations rather than the value of your backyard.

The "Property Trap" is a common hurdle where traditional institutions force you to gamble your family's stability for the sake of business growth. In high-development areas like Thornhill Park, this risk is amplified. As the western corridor expands, your business needs to be agile. You shouldn't be weighed down by the fear of losing your house if a project is delayed or a client pays late. Modern lending for the self-employed has shifted toward these flexible models because they recognise that your business is an entity in its own right.

The Risk of Secured Lending for Sole Traders

Tangling your personal and business assets creates long-term financial stress that's difficult to manage. When you secure a loan against your home, you're essentially "locking up" your equity. This can severely limit your future borrowing power if you want to renovate your property or invest elsewhere. Unsecured business finance is a tool for protecting personal equity, ensuring your home remains a sanctuary rather than a bargaining chip.

Thornhill Park: A Hub for Independent Contractors

The local landscape in Melbourne’s West is dominated by independent contractors, transport operators, and skilled tradies. Thornhill Park residents are at the heart of a massive growth corridor that demands fast, flexible capital. Traditional bank branches often struggle to understand the nuances of contractor income or the seasonal nature of certain trades. Working with a broker who understands the Melton Shire economic zone means you're talking to someone who knows your market. We help you bypass the rigid requirements of big banks, focusing on the equipment and contracts that actually drive your revenue.

How Unsecured Business Finance Works for Self-Employed Australians

Securing a business loan without property security Thornhill Park relies on a fundamental shift in how lenders assess risk. Instead of demanding a mortgage over your home, modern providers look directly at your business's health. They analyse your cash flow, daily bank statement balances, and overall turnover. This data-driven approach allows for much faster decisions, often within 24 to 48 hours, because it bypasses the lengthy property valuation process required by traditional banks. You're judged on the strength of your trade, not the size of your mortgage.

Some business owners worry that "unsecured" implies a lack of regulation or higher risk. In reality, these products are strictly governed by Australian financial laws and often mirror the structure of government-backed business loans that supported SMEs during recent economic shifts. The primary difference is the security type. Instead of a house, lenders often use the Personal Property Securities Register (PPSR). This register allows a lender to record an interest in specific business assets, such as a vehicle or a piece of machinery, without ever touching your personal residential title. It's a transparent and standard practice that protects both parties without risking your family's roof.

Cash Flow-Based Lending vs. Asset-Backed Finance

Cash flow loans are designed for immediate needs like purchasing stock or funding a marketing campaign. They provide working capital based on your projected revenue. However, if you're looking to expand your fleet or upgrade tools, Asset Finance for Self Employed is often the superior path. It uses the equipment itself as the security. This keeps your personal property entirely out of the equation while providing competitive rates for Thornhill Park's growing tradie and transport community. If you're ready to see what's possible, you can explore your finance options with a specialist who understands your trade.

The Advantage of Low-Doc Options

In 2026, being self-employed shouldn't mean being unfinanceable. Low-doc options have evolved significantly. You no longer need three years of reconciled tax returns to prove your worth. Modern lenders prioritise current cash flow over historical tax data to support growing businesses. By using secure digital links to your business bank account, lenders can verify your income instantly. This is particularly helpful for contractors in Melbourne's West who may have complex income streams that don't fit into a standard bank's box.

The typical loan terms for these products generally range from one to five years. Repayment schedules can often be tailored to match your business's seasonal peaks, providing a level of flexibility that traditional fixed-term mortgages simply cannot offer. This ensures your repayments remain manageable even during quieter months.

Asset Finance vs. Unsecured Loans: Which Suits Your Thornhill Park Business?

Choosing the right structure for your funding is just as critical as the capital itself. While a general business loan without property security Thornhill Park offers incredible flexibility for day-to-day operations, asset finance provides a more targeted, often cheaper alternative for those looking to acquire physical equipment. The key difference lies in what the lender holds as security. In asset finance, the vehicle or machine you're buying acts as the collateral, whereas a general unsecured loan relies entirely on your business's creditworthiness and cash flow. Because the lender has a specific claim on the asset, interest rates are typically more competitive than those of a purely unsecured cash injection.

For many local business owners, the tax advantages of asset finance structures are a major drawcard. A Chattel Mortgage, for instance, often allows you to claim the GST on the purchase price in your next BAS, while also providing interest and depreciation deductions throughout the loan term. Hire Purchase arrangements offer a different set of benefits, often suited to specific cash flow requirements or accounting preferences. We always recommend matching your loan term to the "useful life" of the asset. If you're buying a ute that you'll replace in five years, a five-year term ensures you aren't paying for a "ghost" asset once it's retired from your fleet.

When an Unsecured Cash Loan Makes Sense

Sometimes, your growth isn't tied to a piece of machinery. If you're hiring new staff to keep up with Thornhill Park's development boom or launching a digital marketing campaign to capture local leads, an unsecured cash loan is the right choice. These loans cover intangible growth and temporary cash gaps. The primary advantage is speed. Funds can often hit your account within 24 to 48 hours, allowing you to move faster than your competitors. For a deeper look at your options, you might find our Commercial Asset Finance guide helpful for broader context.

Why Asset Finance is the Preferred Choice for Tradies

Tradies in Melbourne’s West often prefer asset finance because it protects their hard-earned cash reserves. Instead of tipping fifty thousand dollars into a new ute, you can keep that money for your operating expenses and pay for the vehicle as it generates income. This "self-securing" nature is perfect for those who want to keep their home equity completely untouched. It’s a common path for local owner-drivers, and we’ve seen a surge in Self-Employed Truck Finance as the logistics hub in the Melton Shire continues to expand.

Qualifying for No-Property Security Finance in Melbourne’s West

Securing a business loan without property security Thornhill Park is more achievable than many sole traders realise. While big banks often get stuck on rigid, outdated criteria, specialist lenders look for signs of a healthy, functioning business. To prepare your application and increase your chances of a fast approval, follow this five-step checklist:

- Verify your ABN: Most lenders prefer an ABN that has been active for at least six to twelve months, though paths exist for newer registrations.

- Review your turnover: Consistent monthly revenue is the primary indicator of your ability to repay the facility.

- Separate your accounts: Using a dedicated business bank account instead of a personal one is vital for a clear credit assessment.

- Check your credit health: Even if your credit file is "bruised" from a past setback, being transparent allows us to find a lender that fits your profile.

- Prepare your ID: A valid Australian Driver’s Licence and Medicare card are typically the only baseline requirements for identification.

Your ABN age is a significant factor, but it isn't always a deal-breaker. If you're operating with a "New ABN," you might still qualify for certain tiers of finance if you can show previous experience in your industry. Lenders want to see that you know your trade and have a reliable pipeline of work in the Melton growth corridor. Demonstrating serviceability through consistent turnover is often more important to a modern lender than how long you've been registered for GST.

Documentation Requirements for 2026

The days of lugging a shoebox of receipts to a bank branch are over. In 2026, digital bank statement technology allows lenders to verify your business performance in minutes. This secure process provides a real-time snapshot of your cash flow, often replacing the need for years of historical tax returns. For many asset-based tiers, a valid ABN and photo ID are the only "hard" documents required to get the ball rolling. You can find a detailed list of what's needed in our guide to Equipment Finance for Sole Traders. If you're ready to see what you qualify for, you can apply for your business finance online today.

The "Local Advantage" in Credit Assessment

Lenders are increasingly looking at the geographic context of a business to determine risk. Operating in high-growth zones like Rockbank, Aintree, and Thornhill Park sends a strong signal of opportunity. Being part of the massive Melbourne West construction and infrastructure boom can work in your favour during the credit assessment. Lenders recognise that businesses in these areas often have access to a steady stream of local contracts and major development projects. Geographic stability can be a positive signal for non-bank lenders. It suggests your business is positioned exactly where the demand is, making you a more attractive prospect than an enterprise operating in a stagnant market.

Quick Choice: Your Specialist Broker for Thornhill Park Business Finance

Bridging the gap between a big bank's rigid policies and your real-world business needs is where we excel. Quick Choice acts as a vital partner for self-employed professionals, ensuring you don't have to compromise your personal assets for professional growth. When you're looking for a business loan without property security Thornhill Park, you need more than just a list of interest rates. You need a specialist who understands that your time is best spent on the tools, not deciphering complex lending criteria. We take on the heavy lifting of the application process, acting as your reliable guide from the first enquiry to the final settlement.

Our deep roots in the western suburbs, including Truganina, Melton, and the surrounding growth corridors, give us a unique perspective. We aren't a faceless online "lending bot" that relies on generic algorithms. Instead, we offer a tailored brokerage service that understands the local economic climate. We know the value of the contracts being signed in the Melton Shire and the potential of the businesses operating out of Thornhill Park. This local expertise allows us to position your business in the best possible light to our panel of specialist lenders, focusing on your future potential rather than just your past tax returns.

Bespoke Solutions for Every Trade

We recognise that no two businesses are identical. Whether you're a sparky based in Tarneit needing a new van or a courier in Hoppers Crossing looking to expand your fleet, we have a clear path forward. We organise your application to highlight your specific business strengths, such as consistent turnover or a strong contract pipeline, rather than focusing on what you don't have. For those just beginning their journey, our Asset Finance for Startups Australia guide provides a dedicated roadmap for new ventures looking to hit the ground running in 2026.

Getting Started is Simple

We've streamlined our process to respect your schedule. Our initial consultation takes as little as two minutes and is designed to give you a clear understanding of your options without any pressure. There are no upfront fees to speak with our team, and our initial chat has no impact on your credit score. We believe in providing transparent, supportive advice that empowers you to make the right decision for your future. You can Organise your Thornhill Park business finance with Quick Choice today and take the first step toward securing the capital your business deserves.

Empower Your Business Growth in Thornhill Park

Securing the capital to expand shouldn't mean putting your family's future on the line. As we've explored, the 2026 lending landscape offers powerful alternatives to the traditional property trap. By focusing on your business's actual performance and cash flow, you can access the funds needed for new equipment or working capital while keeping your home equity entirely separate. Whether you choose a targeted asset finance structure or a flexible cash flow injection, the key is matching the finance to your specific trade requirements.

At Quick Choice, we specialise in helping self-employed Australians navigate these options with ease. Our deep expertise in Melbourne's West growth corridor means we understand the unique pace of the local market. We offer streamlined low-doc solutions and business loan without property security Thornhill Park options that let you stay focused on your projects while we handle the heavy lifting. Don't let rigid bank policies slow your momentum. Secure your business growth with Quick Choice and take command of your company's future today. Your next chapter of success in the Melton Shire starts with a simple, supportive conversation.

Common Questions About Business Finance in Thornhill Park

Can I get a business loan in Thornhill Park without using my house as security?

Yes, you can access capital based on your business performance rather than your home equity. A business loan without property security Thornhill Park allows you to secure funding by demonstrating consistent cash flow or using a specific business asset as collateral. This ensures your family home remains entirely separate from your professional financial obligations.

What is the maximum I can borrow for an unsecured business loan?

Borrowing limits typically range from $5,000 to over $500,000 depending on the lender and your business turnover. Most providers will assess your bank statements to determine a sustainable repayment level. If your business shows strong, consistent revenue, you're likely to qualify for the higher end of these thresholds.

Do I need to be GST registered to qualify for asset finance?

While being GST registered is a common requirement for many lenders, it isn't always mandatory. Most traditional institutions look for a minimum annual turnover between $75,000 and $100,000. However, specialist brokers can often find alternative paths for growing businesses that haven't yet reached the GST threshold but show strong potential.

How long does the approval process take for no-property security loans?

You can often receive approval within 24 to 48 hours. Because these loans don't require a formal valuation of your residential property, the process is significantly faster than a traditional bank loan. Digital bank statement technology allows lenders to verify your income almost instantly, speeding up the journey from application to settlement.

What are the interest rates for unsecured business finance in 2026?

As of July 2026, interest rates for unsecured business loans in Australia generally start between 8.14% and 12.60% per annum. Your specific rate will depend on your business's risk profile, credit history, and trading length. While these rates are higher than a home-secured loan, they reflect the increased risk the lender takes by not holding property as security.

Can a new ABN holder in Thornhill Park get equipment finance?

Yes, new ABN holders can often secure equipment finance if they can demonstrate relevant industry experience. While many lenders prefer a trading history of at least six to twelve months, some specialist providers offer "start-up" tiers. You might need to provide a larger deposit or show a clear contract for upcoming work to strengthen your application.

Will an unsecured loan affect my ability to get a home loan later?

Any business debt will be factored into your personal serviceability when you apply for a home loan. However, a business loan without property security Thornhill Park has the advantage of leaving your property equity untouched. This means you won't have a secondary mortgage "clogging up" the title deeds when you're ready to buy or refinance your home.

What happens if my business cannot make the repayments?

If your business hits a rough patch, it's vital to communicate with your lender or broker immediately. Most unsecured loans include a director's personal guarantee, meaning you remain responsible for the debt if the business fails. While the lender doesn't have an automatic right to your home, they can take legal action to recover the funds from your business assets or personal finances.