Waiting until your tax returns are perfect before upgrading your vehicle is often the quickest way to stall your business growth. If you're a sole trader or sub-contractor, you likely know the frustration of a bank demanding "full financials" that aren’t ready yet. It’s even worse when you fear that multiple applications might damage your credit score. Finding the right work van finance options shouldn't feel like a gamble with your livelihood.

We understand that your time is better spent on the job than chasing paperwork. This 2026 guide highlights flexible, low-doc structures designed specifically for ABN holders who need to get mobile quickly. You’ll learn how to leverage the current $20,000 instant asset write-off and distinguish between a Chattel Mortgage and an Operating Lease. We provide a clear roadmap to secure a tax-effective approval that respects your cash flow and your unique lifestyle as an independent professional.

Key Takeaways

- Learn why commercial asset finance succeeds where standard consumer car loans fail for independent professionals and small business owners.

- Compare the most flexible work van finance options available in 2026, specifically focusing on the ownership and tax advantages of a Chattel Mortgage.

- Discover how Low Doc and No Doc structures allow you to secure a vehicle through income declarations without needing years of completed tax returns.

- Understand how the age of a van dictates your maximum loan term and interest rate, helping you choose between new and used inventory.

- Access a network of over 70 lenders through a specialist guide to find a bespoke solution that traditional banks often overlook.

Why Standard Car Loans Fail Self-Employed Tradies

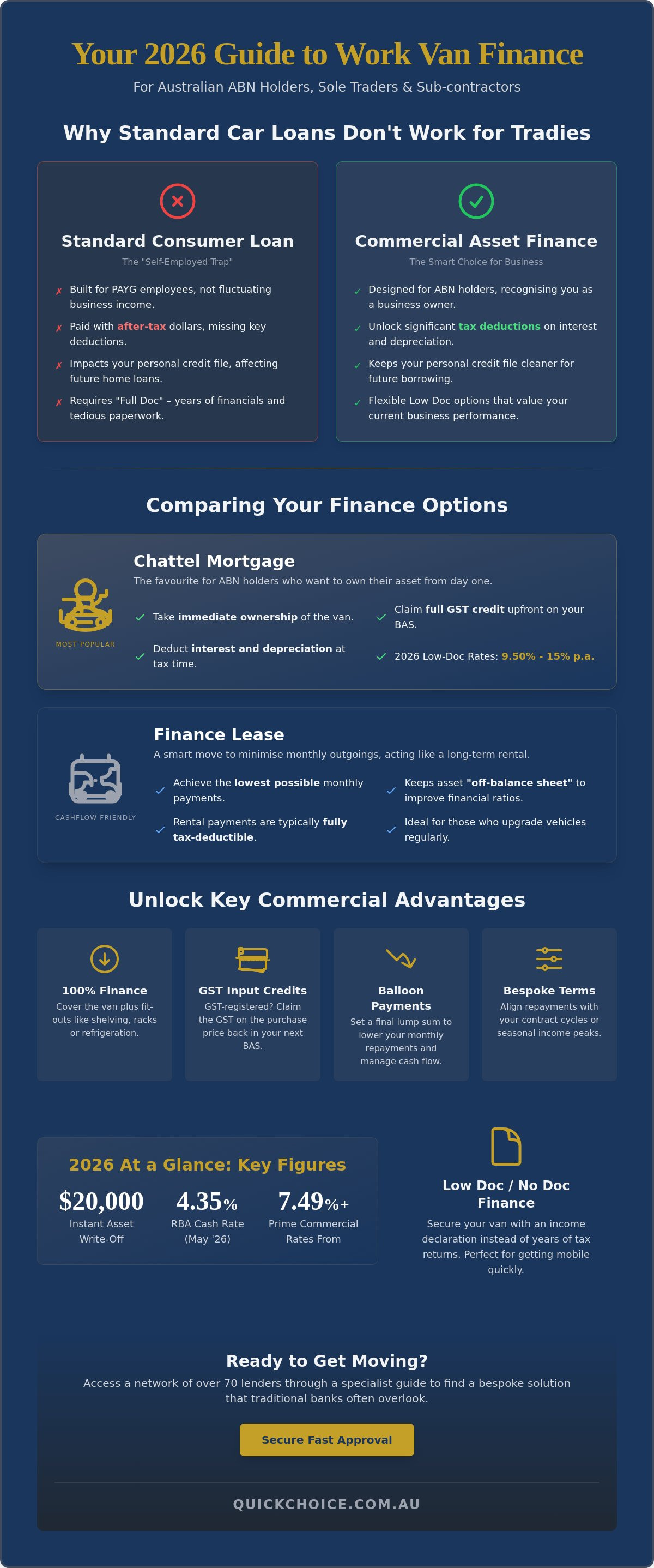

Many ABN holders start their search for a new vehicle by looking at standard consumer car finance options. This is usually where the trouble begins. A personal car loan is designed for PAYG employees with predictable pay slips. It isn't built to handle the fluctuating income or complex tax structures of a small business. When you apply for a consumer loan, big banks often treat you like a risk rather than a professional. This "Self-Employed Trap" leads to automatic rejections simply because your latest tax returns aren't finalised or your income varies between quarters.

Choosing a commercial asset finance structure instead changes how lenders view your application. Rather than looking at you as a consumer who is spending money, they see a business owner investing in a tool for growth. This distinction is vital for your future financial health. A correctly structured commercial loan sits on your business balance sheet. It keeps your personal credit file cleaner, which helps protect your borrowing capacity when you eventually apply for a home loan or personal mortgage. Banks are much more comfortable lending for a house when your personal debt-to-income ratio isn't weighed down by a heavy vehicle loan.

The Problem with Consumer Finance for Business

Personal loans are paid with after-tax dollars. This means you miss out on the significant tax-deductibility that specialised work van finance options provide. Beyond the money, there's the massive time cost. Big banks demand "Full Doc" applications, requiring every bank statement and tax portal printout from the last two years. For a busy contractor, this paperwork is a huge hurdle that stalls progress. Quick Choice bridges this gap by offering finance that recognises your ABN status as a strength. We focus on your current business performance rather than just your history.

Commercial Advantages for ABN Holders

Switching to a commercial structure offers flexibility that personal loans can't match. You can often finance 100% of the van’s purchase price, including necessary fit-outs like specialised shelving, roof racks, or refrigeration units. This keeps your cash in the business where it’s needed most.

- GST Input Tax Credits: If you're GST-registered, you can generally claim the GST on the purchase price back in your next Business Activity Statement.

- Balloon Payments: You can set a final lump sum payment at the end of the term. This lowers your monthly repayments and keeps your daily overheads manageable.

- Bespoke Terms: Commercial work van finance options allow you to align your repayment schedule with your contract cycles or seasonal income peaks.

By treating your van as a business asset rather than a personal luxury, you unlock a level of financial agility that standard bank loans simply won't allow. It’s about making your equipment work as hard for your bank balance as it does on the job site.

Comparing Finance Structures: Which Suits Your Cash Flow?

Selecting from the available work van finance options requires a clear understanding of your business's cash flow needs. While a low interest rate is attractive, the tax structure often has a bigger impact on your bottom line. As of May 2026, the official RBA cash rate sits at 4.35%, which has pushed commercial vehicle finance rates to start from approximately 7.49% p.a. for prime borrowers. In this environment, choosing a structure that aligns with your BAS cycle and depreciation schedule is essential for staying ahead.

Most Australian sub-contractors and sole traders choose between three primary paths. Each offers different levels of ownership and tax flexibility. A Chattel Mortgage provides immediate ownership, while a Finance Lease acts more like a long-term rental. A Commercial Hire Purchase (CHP) serves as a middle ground for those wanting equity without immediate ownership hurdles. Understanding these differences helps you avoid committing to a repayment schedule that doesn't fit your income pattern.

Chattel Mortgage: The 2026 Outlook

In 2026, the Chattel Mortgage remains the favourite choice for ABN holders who want to own their gear. You take title of the van immediately, and the lender secures the loan against the asset. If you're registered for GST, this structure allows you to claim the full GST credit on the purchase price upfront. With low-doc rates currently ranging between 9.50% and 15% p.a., the ability to claim both interest and depreciation helps significantly in managing the total cost of ownership.

Leasing and Hire Purchase Nuances

A Finance Lease can be a smart move if you prefer to keep your monthly outgoings as low as possible. It often keeps the asset "off-balance sheet," which can improve your financial ratios when applying for other business credit. If you're weighing up these choices, this government guide to leasing vs. buying offers a neutral look at the long-term implications of each structure.

Commercial Hire Purchase is another option where you pay for the van in instalments and take ownership after the final payment. Both leasing and CHP often utilise balloon payments. This lump sum at the end of the term reduces your monthly pressure, but it requires careful planning for the eventual payout. Speaking with a specialist who understands the sub-contractor lifestyle can help you model these scenarios before you sign any contracts.

Navigating Low Doc and No Doc Van Finance

For many self-employed Australians, the biggest barrier to upgrading a fleet isn't the cost, but the paperwork. Traditional lenders often demand two years of audited tax returns to prove your income. Low Doc work van finance options remove this hurdle. They allow you to secure a vehicle by "self-declaring" your income. This means you provide a signed statement confirming your business earns enough to cover repayments, often backed by just a few months of bank statements or a recent BAS. It's a streamlined path that respects the reality of a busy contractor's life.

No Doc finance goes one step further by bypassing income verification entirely. It isn't available to everyone; it usually hinges on specific "trust indicators" that reduce the lender's risk. Lenders look for borrowers who own property or have a long, clean credit history. If you meet these criteria, you might find a path to no doc business vehicle finance that requires almost no financial disclosure. This is particularly useful if your business is growing rapidly and your last tax return no longer reflects your current earning power.

Your ABN is the central piece of this puzzle. Most specialist lenders prefer an active ABN for at least 12 to 24 months. This history proves your business is stable and past the initial "startup" phase. If your ABN is younger than a year, approval is still possible, though you may need to provide a larger deposit to offset the lack of trading history.

The Self-Employed Documentation Checklist

While these work van finance options require less paperwork, you still need to be organised. Having these items ready will speed up your approval:

- Active ABN: Ideally held for 12+ months and GST registered.

- Proof of Identity: A current Australian Driver's Licence.

- Income Declaration: A signed form stating your annual business income.

- Clean Credit File: Ensure your bills and existing loan repayments are up to date before applying.

Overcoming the "New Business" Hurdle

If you’ve been trading for less than 12 months, you're in the "new business" category. Lenders see more risk here because they can't see a full year of seasonal cycles. A common strategy to gain approval is providing a deposit of 20% or more. This reduces the lender's exposure and shows you have skin in the game. For a deeper look at navigating these specific requirements, check out our guide on vehicle finance for contractors. It breaks down how to position your ABN for the best possible rates.

Strategic Considerations: New vs. Used and Tax Implications

Choosing between a showroom-fresh vehicle or a reliable second-hand unit involves more than just the sticker price. The age of the van is a primary factor in your work van finance options. Most lenders apply an "Age of Asset" rule; they generally require the vehicle to be no older than 12 years at the end of your loan term. If you purchase a six-year-old van, you might be restricted to a four or five-year term. New vans typically attract the lowest interest rates, starting from approximately 7.49% p.a. for prime borrowers, and offer the security of a manufacturer’s warranty.

Used vans provide a lower entry point and slower depreciation, but you should prepare for interest rates that are often higher than new vehicle rates. Maintenance costs also tend to rise as the odometer climbs. For the 2025 to 2026 financial year, the instant asset write-off threshold is $20,000. This allows small businesses with an aggregated turnover of less than $10 million to immediately deduct the full cost of eligible assets. To qualify, the asset must be first used or installed ready for use by 30 June 2026. This makes the timing of your purchase critical for your next tax return.

Financing the Full Fit-Out

A van is rarely "work-ready" the moment it leaves the dealership. You likely need specialised shelving, refrigeration, roof racks, or custom signage to make the vehicle functional. Including these costs in your initial asset finance is a smart move. It allows you to wrap the entire "ready-to-work" cost into a single monthly repayment. This preserves your cash flow and ensures your fit-out is covered by the same professional structure as the vehicle itself. Quality fit-outs can also help maintain the van’s resale value, which is a vital consideration if you have a balloon payment due at the end of your term.

Tax Benefits and GST Credits

You can generally claim the full GST on the purchase price back in your next Business Activity Statement, up to the maximum credit limit of $6,334 for the 2025 to 2026 year. While interest and depreciation are typically deductible under a Chattel Mortgage, lease payments are handled as a rental expense. The car depreciation limit for the 2025 to 2026 income year is $69,674; this is the maximum value you can use for these calculations. We recommend you consult a qualified accountant to maximise your specific 2026 tax position based on these current thresholds. If you’re ready to see how these numbers apply to your business, explore our bespoke asset finance solutions today and get a clearer picture of your borrowing power.

Securing Fast Approval with a Local Specialist

Choosing the right vehicle and tax structure is only half the battle. The final step is finding a lender who actually understands the grit and hustle of the Melbourne West industrial hubs. While big banks offer one-size-fits-all portals, they often lack the nuance required for complex ABN applications. Our team brings local expertise to Truganina and Werribee, ensuring your application is positioned for success from the very first submission. We know that a rejection isn't just a "no"; it can lead to a "rejection loop" that unnecessarily marks your credit file.

The Quick Choice advantage lies in our breadth of reach. We provide access to over 70 lenders, many of whom don't deal directly with the public. This competition works in your favour, allowing us to source work van finance options that match your specific credit profile and business age. For a comprehensive look at the broader market, our parent pillar on business vehicle finance australia offers an essential roadmap for self-employed buyers in 2026.

Tailored Support for Melbourne West Tradies

Contractors in Rockbank, Melton, and Caroline Springs face unique logistical challenges. You need a partner who knows the local landscape and the specific requirements of your trade. A faceless national lender won't understand why a courier driver needs a different repayment structure than a sparkie or a plumber. We take the time to learn your business model. This ensures your finance supports your growth rather than hindering it. Our local focus means we're familiar with the heavy-duty requirements of Melbourne West businesses, from refrigeration units to custom tool racking.

Next Steps: From Application to Ignition

We value your time. Our goal is to move you from the first chat to a 24-48 hour approval window as smoothly as possible. We take over the heavy lifting, managing the paperwork and lender negotiations so you can stay on the tools and keep your jobs moving. Once your finance is secured, you can focus on what you do best while we handle the settlement details. When you're ready to upgrade your fleet without the stress of bank queues, Organise a quote with Quick Choice today. Let's get your business the mobility it deserves.

Drive Your Business Forward in 2026

You now have a clear understanding of how the right commercial structure protects your home loan capacity while maximising your tax position. By moving away from standard bank loans and embracing flexible work van finance options, you can secure the equipment you need without the stress of "full doc" requirements. Whether you're eyeing a new van with a full warranty or a used asset that fits your immediate budget, the 2026 landscape offers plenty of room for growth.

Quick Choice is here to help you navigate this path with quiet confidence. We provide local support across Melbourne West and offer expertise in specialised Low Doc and No Doc ABN loans. With access to over 70 specialist lenders, we ensure your application is matched with the right provider from the start. This approach removes the obstacles that often stall independent professionals and sub-contractors.

Don't let paperwork stall your momentum. Get a Tailored Van Finance Quote from Quick Choice and let us handle the heavy lifting while you stay focused on your clients. We're ready to help you get behind the wheel and grow your business today.

Frequently Asked Questions

Can I get work van finance with a new ABN?

Yes, you can secure finance with a new ABN, though lenders generally view startups as higher risk. If your business has been trading for less than 12 months, providing a 20% deposit often helps bridge the gap. This shows the lender you have skin in the game while helping you access competitive work van finance options that might otherwise be restricted to established businesses.

What is the difference between a Chattel Mortgage and a van lease?

The main difference lies in ownership and tax timing. With a Chattel Mortgage, your business owns the van from day one, allowing you to claim the full GST credit upfront in your next BAS. A lease functions more like a long-term rental where the lender retains ownership; you make monthly payments that are usually fully tax-deductible as an operating expense.

Do I need a deposit for a business van loan in Australia?

You don't always need a deposit for a business van loan. Many established ABN holders with clean credit can qualify for 100% finance, which can even include fit-out costs like shelving and signage. However, a deposit is a useful tool to lower your monthly repayments or to secure an approval if you are a new business or have a complex credit history.

Is work van finance tax-deductible for sole traders?

Yes, work van finance is highly tax-effective for sole traders. You can generally claim the interest on the loan and the vehicle's depreciation as business expenses. For the 2025 to 2026 financial year, you can also take advantage of the $20,000 instant asset write-off for eligible vehicles, provided they are ready for use by 30 June 2026. This is one of the most popular work van finance options for those looking to reduce their taxable income.

Can I finance a used van from a private seller?

Yes, you can finance a used van from a private seller, though the process involves a few extra steps compared to a dealership. Lenders typically require an independent inspection and a valuation to ensure the van is worth the loan amount. They also perform a PPSR check to confirm the vehicle has no hidden debt before they transfer funds to the seller's account.

What happens to my finance if I want to upgrade my van in two years?

Upgrading your van before the loan term ends is a common practice for growing businesses. You will need to "pay out" the existing loan, which includes the remaining principal and any balloon payment. Most tradies use the trade-in value or sale price of the old van to cover this payout before starting a new agreement for their next vehicle.

How does a balloon payment affect my monthly repayments?

A balloon payment significantly lowers your monthly repayments by deferring a large percentage of the loan principal until the end of the term. While this improves your daily cash flow, you must plan for that final lump sum. At the end of the term, you can choose to pay it out in full, refinance the balloon amount, or trade in the van to cover the cost.

Will applying for van finance affect my personal credit score?

Applying for finance will result in a "hard inquiry" on your credit report, which can temporarily affect your score. This is why it is vital to avoid sending applications to multiple banks at once. Working with a specialist broker ensures your application goes to the lender most likely to approve you the first time, protecting your credit file from unnecessary damage.