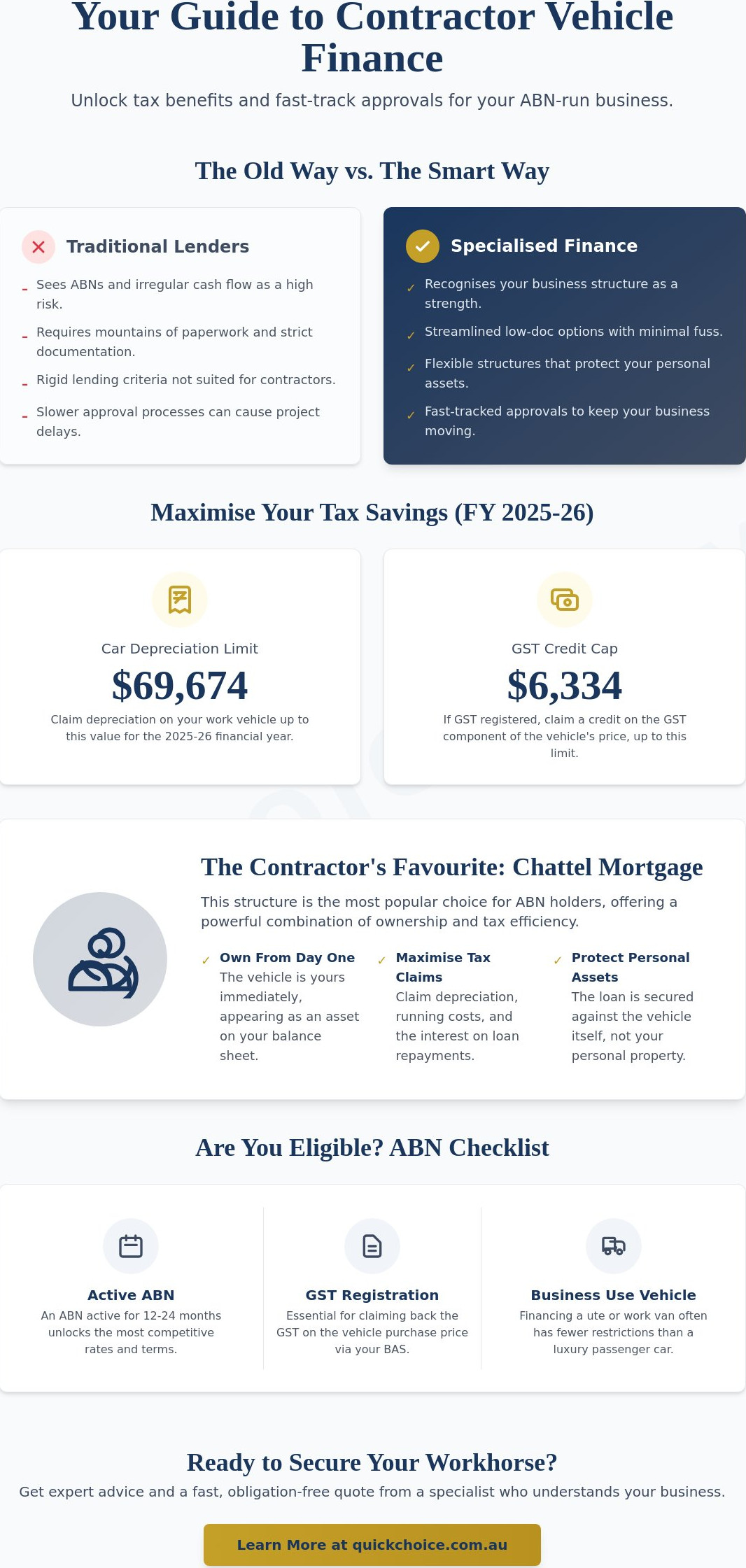

Why should your bank treat your thriving ABN business like a financial risk simply because you don't have a standard payslip? It's a common frustration for independent professionals who need reliable transport but face mountains of paperwork and rigid lending criteria. We understand that irregular cash flow can make long-term commitments feel daunting, especially when you need to secure vehicle finance for contractors quickly to stay on the job and maintain your momentum.

You deserve a finance partner who recognises that your business structure is a strength, not a weakness. This guide promises to help you master the complexities of contractor finance by explaining how to use ABN structures and tax benefits to your advantage. We will show you how to achieve fast-tracked approvals with minimal fuss while protecting your cash flow. You will learn about the current $69,674 car depreciation limit for the 2025-26 financial year, the $6,334 GST credit cap, and how to choose a loan structure that fits your specific tax strategy. From chattel mortgages to the latest FBT exemptions for electric vehicles, we provide the clarity you need to move forward with confidence.

Key Takeaways

- Understand why a Chattel Mortgage is often the preferred choice for ABN holders to own their asset from day one while unlocking significant tax advantages.

- Learn how to navigate vehicle finance for contractors by leveraging specialised low-doc options that bypass the rigid documentation requirements of major banks.

- Discover how to maximise your business cash flow by correctly claiming interest costs and depreciation through the latest tax-effective strategies.

- Identify the critical differences between Finance Leases and Commercial Hire Purchases to ensure your loan structure aligns with your long-term business goals.

- Gain insights into how a specialist asset finance partner provides the local expertise needed to secure fast approvals for Melbourne-based independent professionals.

Understanding Vehicle Finance for Contractors in Australia (2026)

Vehicle finance for contractors isn't just a standard car loan with a different label. It is a specialised category of asset finance designed specifically for ABN holders who use their vehicles as essential business tools. Whether you're a tradie in a Hilux or a consultant visiting clients, the way you fund your transport affects your tax position and your bottom line. When you're self-employed, your vehicle is often your most important piece of equipment, and the finance structure should reflect that reality.

Standard consumer car loans often fall short for independent professionals. Most big banks build their lending models around steady PAYG income and identical fortnightly payslips. If your income fluctuates or you've recently transitioned to full-time contracting, traditional lenders might see you as a higher risk. Specialised vehicle finance for contractors recognises your business's potential instead. This approach often grants you access to commercial interest rates, which can be more competitive than retail options because the loan is secured against a business asset.

Why Contractors Need Specialised Finance

Traditional lenders often struggle to understand the rhythm of a contractor's life. They want to see a predictable financial history that simply doesn't exist when you're managing multiple projects or seasonal work. Specialised finance bridges this gap by looking at your business's overall health rather than just a weekly snapshot. This allows for more flexible repayment structures that can align with your specific cash flow patterns.

Separating your personal debt from your business assets is another critical move. By keeping your vehicle finance under your ABN, you protect your personal borrowing capacity for things like home loans. Most of these arrangements use the vehicle itself as security. You can find this Chattel Mortgage Explained in detail online, but essentially, it means the lender takes a mortgage over the asset. This structure typically allows for lower rates and faster approvals without risking your personal property or requiring a massive deposit.

ABN Requirements and Eligibility in 2026

To qualify for these business-focused products, your ABN is your most important credential. Most lenders prefer an ABN that has been active for at least 12 to 24 months. While some "New ABN" products exist for those with 6 months of trading history, having a two-year history usually unlocks the most competitive terms and higher borrowing limits. It shows the lender that your business is stable and capable of meeting its commitments.

Your GST status also plays a significant role in your borrowing power. If you're registered for GST, you can often claim the GST component of the vehicle's purchase price back on your next BAS, which provides an immediate cash flow boost. This is a core part of the asset finance for self employed framework that helps independent professionals grow. Additionally, the type of vehicle you choose matters. Financing a "workhorse" ute often comes with fewer restrictions than a luxury passenger car, as the ATO views certain vehicles as inherently business-related, simplifying your depreciation claims and fringe benefits tax considerations.

Choosing the Right Finance Structure for Your Business Vehicle

Selecting the right finance structure is a strategic decision that directly impacts your monthly overheads and tax position. For independent professionals, the choice usually boils down to whether you want to own the asset outright or maintain the flexibility to upgrade frequently. Matching your loan structure to your specific cash flow is the secret to successful vehicle finance for contractors. Most lenders offer terms ranging from one to seven years, allowing you to align your repayments with the expected working life of your vehicle.

The Chattel Mortgage: The Contractor’s Favourite

The Chattel Mortgage remains the most popular choice for Australian contractors because it offers the benefits of ownership from day one. Under this arrangement, you own the vehicle immediately, and the lender secures the loan against the asset. Specifically, a Chattel Mortgage is an asset-backed loan where the vehicle acts as security. This structure is particularly effective for those looking to maximise their tax position early on.

If your business is registered for GST, you can generally claim the full GST amount of the vehicle's purchase price as an Input Tax Credit on your next Business Activity Statement (BAS). This provides a significant cash flow injection right when you need it most. Additionally, you can often apply the ATO Instant Asset Write-Off or claim depreciation and interest costs as deductions, provided the vehicle is used for business purposes. For many, this combination of ownership and immediate tax relief makes it the gold standard for asset acquisition.

Leasing vs. Buying: Which Suits Your Cash Flow?

While ownership suits many, leasing offers a different set of advantages for contractors who prefer a "set and forget" approach. An operating lease is ideal if you plan to upgrade your vehicle every three years to keep your business image modern and avoid out-of-warranty repair costs. You essentially pay for the use of the vehicle rather than the vehicle itself. Conversely, a Commercial Hire Purchase (CHP) allows you to hire the vehicle for a fixed term with the option to purchase it at the end, which can be useful for those not registered for GST.

Balloon payments, also known as residual values, are a powerful tool to manage your monthly commitments. By deferring a percentage of the loan principal to the end of the term, you can significantly lower your ongoing monthly repayments. This is a smart move for sub-contractors who need to keep their fixed costs low to navigate periods of irregular income. If you're unsure which path fits your current contract, seeking specialist asset finance guidance can help clarify which structure protects your cash flow best. Your decision should ultimately depend on your annual kilometres, your maintenance preferences, and how long you intend to keep the vehicle on the road.

Low Doc and No Doc Options for Fast-Paced Contractors

Speed is everything when a contract is on the line. If you've ever been knocked back by a bank because your latest tax returns are still with your accountant, you'll know how frustrating the traditional lending process can be. In the 2026 lending environment, "Low Doc" options have evolved to meet the needs of independent professionals who have the cash flow but lack the paperwork. This specialised approach to vehicle finance for contractors prioritises your current business performance over historical data that might be eighteen months out of date.

For many, no doc business vehicle finance represents the gold standard for efficiency. To qualify for a true "No Doc" loan, lenders typically look for three key markers of stability. First, they prefer an ABN that has been active for at least two years. Second, a clean personal credit history is essential. Third, being a property owner (or having a mortgage) significantly increases your chances of approval. When these boxes are ticked, lenders are often happy to provide finance based on a simple self-declaration of income, bypassing the need for financial statements entirely.

Qualifying Without Recent Tax Returns

If you don't meet the strict No Doc criteria, Low Doc remains a powerful alternative. Instead of full tax returns, lenders may ask for your most recent Business Activity Statements (BAS) or three months of bank statements. They use these to verify that your business has consistent turnover and can comfortably manage the repayments. Maintaining a "clean" bank account for at least three to six months is vital; this means avoiding late fees or overdrawn events that could signal cash flow stress. Low Doc loans allow contractors to secure assets based on current performance rather than historical data.

The Impact of Credit Scores on Contractor Loans

Your personal credit file acts as the gateway to your business finance. Even though the loan is for your ABN, lenders view your personal financial behaviour as a reflection of how you'll manage business debt. It's a good idea to clean up your credit before applying by closing unused credit cards and ensuring all utility bills are paid on time. In 2026, most specialist lenders use "soft" credit enquiries to provide initial quotes. This is a massive advantage because it allows you to see your eligibility without leaving a mark on your file. A "hard" enquiry, which can temporarily lower your score, only occurs once you move to a formal application. Protecting your score ensures you keep access to the most competitive commercial rates available.

Maximising Tax Efficiency and Business Cash Flow

Mastering vehicle finance for contractors means looking beyond the interest rate to see the full tax picture. When you're self-employed, every dollar counts, and how you structure your loan can significantly reduce your net cost. By aligning your purchase with Australian tax incentives, you transform a necessary business expense into a strategic growth tool. Beyond the loan itself, you can also bundle fuel, maintenance, and insurance into your business budget, ensuring your on-road costs remain predictable and tax-deductible.

The 2026 Instant Asset Write-Off Landscape

The ability to reduce your taxable income through asset depreciation is a major advantage of business-purpose financing. For the 2025-26 financial year, the maximum value used for calculating depreciation on a passenger vehicle is $69,674. If you're registered for GST, you can generally claim an upfront credit of up to $6,334, which provides an immediate boost to your business bank account. These incentives are designed to encourage investment, but they require the right loan structure to be effective.

Using a Chattel Mortgage allows you to claim these benefits early, often in the same financial year as the purchase. This is particularly useful if you've had a high-income year and need to offset your tax liability. Because these thresholds and rules can shift, you should consult our business vehicle finance australia guide for the most current updates on turnover requirements and eligibility. Getting the timing right can save your business thousands in potential tax payments.

Structuring Repayments to Match Project Cycles

Contractors in industries like landscaping or construction often face seasonal ebbs and flows in their income. Standard monthly repayments don't always suit this reality. We focus on flexible structures that allow you to match your repayments to your project cycles. For example, making a larger initial deposit can reduce your Loan to Value Ratio (LVR), which often leads to more favourable terms and lower ongoing interest costs.

Balloon payments are another essential tool for preserving your monthly cash flow. By deferring a portion of the vehicle's cost to the end of the term, you keep your regular commitments manageable. This leaves more capital available for other business expenses, such as hiring extra hands or purchasing materials for a new contract. If you want to see how these structures could benefit your specific ABN setup, get in touch with our asset finance specialists today to explore your options.

Securing Your Workhorse with Quick Choice Melbourne

Securing the right vehicle shouldn't be the hardest part of your job. While the big banks often rely on rigid algorithms that don't account for the unique nature of self-employment, we take a different approach. As a specialist broker, we bridge the gap between your ABN business and a panel of over 30 leading lenders who understand the value of independent professionals. This access allows us to find the most competitive vehicle finance for contractors, tailored specifically to your trade and tax strategy.

Our "Fast-Track" process is designed for speed because we know that being off the road means losing money. From your initial enquiry to having the keys in your hand, we aim for a turnaround of 24 to 48 hours. You won't be stuck in a phone queue or treated like a data point. Instead, you'll work with a guide who understands that your ute or van is the heartbeat of your business. We handle the heavy lifting of the application so you can stay focused on your clients.

Local Expertise for Melbourne’s West

We are deeply embedded in the growth of Melbourne's western corridor. Whether you are a tradie building the new communities in Aintree and Rockbank or a contractor based in Truganina, Melton, or Werribee, we know your local market. We offer on-site visits in Hoppers Crossing or Tarneit to discuss your business needs in person, ensuring we understand the practicalities of your operation. This local knowledge is vital, especially for those in the transport and construction industries in Melton where project demands can shift quickly. We don't just work in the area; we support the people who are building it.

The Quick Choice Advantage

Choosing us means gaining a partner who values your time as much as you do. We combine the ease of streamlined digital applications with the reassurance of genuine human expertise. We don't just find you a loan; we help you organise a structure that maximises your tax effectiveness, building on the strategies we've discussed regarding depreciation and cash flow. Our goal is to remove the obstacles standing between you and your next business asset. We take pride in being a reliable specialist guide for every client we serve. Get a personalised contractor vehicle finance quote today and experience a smoother, faster path to securing your next workhorse.

Drive Your Business Forward with Confidence

Securing the right vehicle shouldn't be a source of stress for independent professionals. By selecting a finance structure that aligns with your specific cash flow and leveraging the tax benefits of the 2025-26 financial year, you can turn a necessary expense into a powerful business asset. Whether you're utilising low-doc options to bypass traditional bank red tape or choosing a Chattel Mortgage to maximise your GST credits, the right strategy keeps your business moving without draining your capital. Mastering vehicle finance for contractors is about more than just getting the keys; it's about building a sustainable foundation for your future growth.

Our team of local experts in Melbourne’s West is ready to help you navigate this process with ease. We provide access to a specialist ABN lending panel and focus on fast-tracked 48-hour approvals to ensure you stay on the job. You don't have to tackle complex financial decisions alone when you have a reliable specialist guide by your side. Secure your next work vehicle with Quick Choice’s specialist contractor finance and take the next step in your professional journey. We're here to help you build the business you've always envisioned.

Frequently Asked Questions

Can I get vehicle finance if I have only had my ABN for 6 months?

Yes, you can secure finance with a 6-month ABN, though your options may be more restricted compared to established businesses. While many lenders prefer a trading history of 12 to 24 months, specialised products exist for newer contractors. You might need to provide additional proof of income, such as recent bank statements or a signed contract for upcoming work, to demonstrate your ability to manage the repayments confidently.

What is the difference between a personal car loan and a business vehicle loan?

The primary difference lies in the vehicle's usage and the available tax benefits. A business vehicle loan is designed for assets used more than 50% of the time for business purposes, allowing you to claim interest and depreciation as deductions. Unlike personal loans, these commercial products often offer structures like Chattel Mortgages, which are specifically built to support an ABN holder's cash flow and long-term business growth.

Do I need to be GST registered to get a contractor vehicle loan?

No, you don't need to be GST registered to qualify for a contractor vehicle loan. However, being registered allows you to claim the GST on the purchase price back as an Input Tax Credit on your next BAS, which provides a significant cash flow boost. If you aren't registered, structures like a Hire Purchase might be more suitable, as they cater to businesses that don't need to claim GST credits upfront.

How much deposit does a contractor typically need for a work ute?

Many contractors can secure a work ute with a $0 deposit, provided they have a strong credit history and an established ABN. While not always required, contributing a 10% to 20% deposit can lower your Loan to Value Ratio (LVR), which often results in a more competitive interest rate. This also reduces your monthly repayments, helping you maintain a healthier cash flow during quieter project cycles or between major contracts.

Can I finance a used vehicle as a sub-contractor?

Yes, you can certainly finance a used vehicle to help grow your business. Lenders typically have age restrictions, often requiring the vehicle to be no older than 12 years by the end of the loan term. Financing a used workhorse is a common way for sub-contractors to access vehicle finance for contractors without the higher price tag of a brand-new model, provided the asset is in good mechanical condition and meets lender criteria.

What documents do I need for a Low Doc vehicle loan in 2026?

In 2026, Low Doc loans typically require your ABN details, a valid driver's licence, and alternative proof of income such as recent Business Activity Statements (BAS) or three months of bank statements. You won't need to provide full, finalised tax returns or profit and loss statements. This streamlined documentation makes it much easier for contractors with unfinalised accounts to secure the equipment they need to stay on the job and keep working.

Is the interest on my contractor vehicle loan tax-deductible?

Yes, the interest component of your loan repayments is generally tax-deductible to the extent that the vehicle is used for business purposes. If you use your vehicle 80% for work and 20% for personal use, you can claim 80% of the interest costs as a legitimate business expense. This deduction, combined with depreciation claims under current ATO limits, significantly reduces the overall cost of financing your work vehicle over the life of the loan.

How long does the approval process take for contractors?

The approval process is remarkably fast when working with a specialist, often taking between 24 and 48 hours from enquiry to finalisation. While big banks can take weeks to process self-employed applications, our streamlined digital systems allow for rapid matching with suitable lenders. Once you provide the basic documentation for vehicle finance for contractors, we can often secure a conditional approval on the same day, getting you behind the wheel sooner.