Why should your business growth be held hostage by a pile of paperwork that doesn't reflect your current success? If you've spent hours hunting for old tax returns just to be told "no" by a traditional lender, you're certainly not alone. Many self-employed professionals find that big banks simply don't understand the rhythm of independent work. Securing no doc business vehicle finance isn't a last resort for struggling companies; it's a strategic move for established Australian businesses that need to maintain momentum without the administrative burden.

We know that your time is better spent on the tools or with your clients than at a kitchen table sorting through receipts. You deserve a finance partner who values your ABN and your track record over a stack of BAS statements. In this guide, you'll learn exactly how to qualify for a work vehicle upgrade in 2026 using minimal documentation. We'll walk you through the current interest rate landscape, the essential requirements for your ABN, and how to fast-track your approval so you can get back to work with the right gear.

Key Takeaways

- Discover how to bypass the traditional bank paperwork trail by using a finance structure designed specifically for ABN holders and self-employed professionals.

- Identify the three non-negotiable requirements to qualify for no doc business vehicle finance in 2026 without needing to provide tax returns or BAS.

- Learn how to distinguish between no doc and low doc options to ensure you secure the most competitive interest rate for your business circumstances.

- Understand why being "asset-backed" significantly boosts your approval odds and which specific assets lenders value most during the assessment process.

- Find out how a specialist broker can fast-track your vehicle upgrade by connecting your business with a wide panel of flexible commercial lenders.

What is No Doc Business Vehicle Finance?

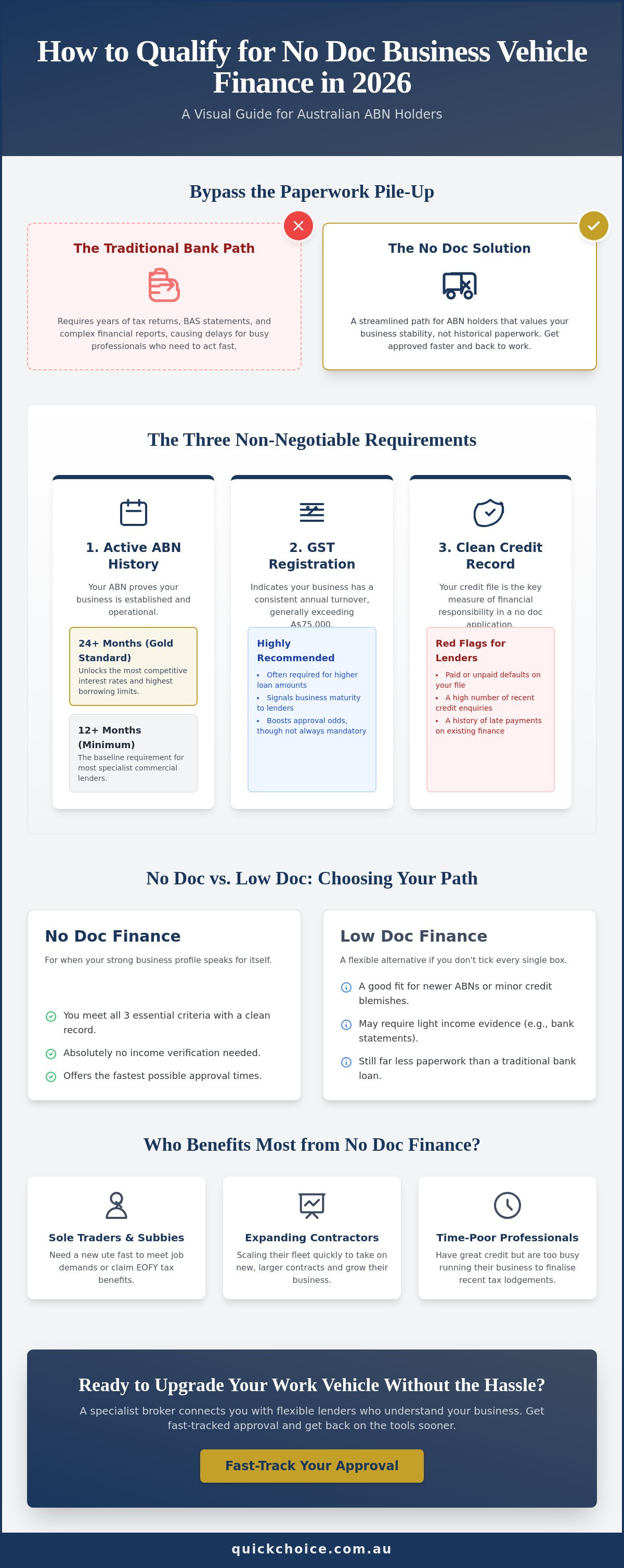

In the Australian commercial lending landscape, no doc business vehicle finance represents a streamlined approach to acquiring essential assets. Unlike traditional bank loans that demand years of tax returns and Profit & Loss statements, these products rely on the inherent value of the vehicle and your professional standing as an ABN holder. Lenders aren't ignoring your financial health; they're simply using different metrics to assess risk. By focusing on your credit history and your business's longevity, they can offer fast-tracked approvals that keep your wheels turning.

Understanding Business loan basics helps clarify why this specific structure works. Most no doc products are secured against the vehicle itself, providing the lender with a tangible safety net. This differs significantly from individual car loans, which are governed by strict consumer lending laws and usually require extensive personal income verification. In 2026, the market has shifted toward digital-first applications. Advanced algorithms now allow specialist lenders to verify your business's legitimacy and creditworthiness in minutes, making the old-fashioned "paperwork mountain" a thing of the past.

The "No Doc" Philosophy for Self-Employed Australians

This lending style prioritises your future potential over your historical data. For many subbies, cash flow is strong but irregular, which can confuse a standard bank manager. The "no doc" approach values your equity and your reputation. It recognises that an established contractor with a clean credit file is a reliable bet, even if their latest tax return hasn't been lodged yet. The Australian market has embraced "Express" commercial lending, where the speed of the transaction is seen as a vital tool for business growth rather than a shortcut. It's about getting you into the driver's seat without the administrative headache.

Who Benefits Most from No Doc Loans?

Several types of professionals find this path particularly effective for their operations:

- Sole Traders: If you need to upgrade your work ute before the end of the financial year to claim tax benefits, speed is everything.

- Expanding Contractors: Businesses in growing hubs like Werribee or Melton often need to scale their fleet quickly to meet new contract demands.

- Busy Professionals: Many established businesses have excellent credit but simply haven't had the time to finalise their most recent BAS or tax filings.

By choosing a no doc pathway, you're opting for a finance solution that respects your schedule and understands the realities of running a modern Australian business. It's a partnership built on trust and practical results.

The Essential Criteria: How to Qualify for No Doc Finance

Qualifying for no doc business vehicle finance isn't about proving your income through historical tax returns; it's about demonstrating your business's stability through three critical pillars. Lenders look at your ABN history, GST status, and credit standing to determine your reliability. While traditional SBA loan requirements often demand years of exhaustive financial history, the Australian commercial market offers a more agile path for those who meet these baseline benchmarks. Specialists use these data points to build a profile of your business's health without needing to see a single Profit & Loss statement.

ABN and GST Registration Requirements

Your ABN is the foundation of your application. Most specialist lenders require an active ABN for a minimum of 12 months, though 24 months is the gold standard for accessing the most competitive interest rates. If your ABN was recently reactivated after a period of cancellation, lenders might treat it as a newly established entity, which can affect your borrowing limits. GST registration is another powerful signal of business maturity. While not always mandatory, being GST-registered often unlocks higher borrowing capacities because it demonstrates a consistent level of annual turnover, generally exceeding A$75,000.

Credit History and the "Clean Record" Rule

In the absence of BAS or tax returns, your credit file does the heavy lifting. Lenders will scrutinise your Veda or Equifax score to look for a pattern of financial responsibility. A clean record is generally non-negotiable for a true no doc approval. Even minor defaults or a high number of recent credit enquiries can shift your application into "low doc" territory, where some proof of income becomes necessary. Maintaining a strong personal credit score is vital, as most commercial lenders view the individual behind the ABN as the ultimate guarantor of the debt. If you're unsure how your current credit standing impacts your options, a quick chat with Quick Choice can help you understand your position.

The 50% Business Use Declaration

To access these commercial products, you must declare that the vehicle will be used for business purposes at least 50% of the time. This declaration is a legal requirement that aligns your finance with Australian tax regulations, allowing for potential GST credits and depreciation claims. Providing a clear and honest "purpose of use" statement ensures your finance remains compliant with commercial lending standards. Beyond the legalities, this declaration often includes a "Signed Income Declaration," where you formally state that your business generates sufficient cash flow to manage the repayments comfortably.

No Doc vs. Low Doc: Choosing the Right Path for Your Business

Choosing between no doc and low doc finance often feels like a balancing act for self-employed Australians. While both paths avoid the exhaustive paperwork of traditional bank loans, they cater to different stages of business readiness. Knowing What You Need To Know About No-Doc Business Loans helps you decide if your current record-keeping is enough to secure a deal. The primary distinction lies in the level of verification required to satisfy the lender's risk assessment. While no doc business vehicle finance relies almost entirely on your ABN history and credit score, low doc options introduce a small amount of evidence to potentially secure more favourable terms.

The trade-off usually centres on speed and privacy versus the total cost of the loan. No doc products offer the ultimate convenience, but they often carry higher interest rates because the lender takes on more perceived risk. If your business has a high turnover but low physical assets, providing a few months of bank statements or an accountant's letter through a low doc application might unlock a lower rate. We help you navigate these choices by assessing your specific situation and matching you with the lender that offers the best balance of speed and value.

When to Choose No Doc (Zero Paperwork)

This path is ideal for urgent purchases where tax returns are not yet lodged or if you simply prefer to keep your financial details private. It's best suited for asset-backed borrowers with high-tier credit scores who need to move quickly. In the fast-paced Australian market, approvals for no doc business vehicle finance can often be secured within 24 to 48 hours. If you've been in business for over two years and own property, this is frequently the most efficient way to get a new ute or van on the road without digging through old files.

When Low Doc is the Smarter Alternative

Low doc finance serves as a middle ground. By providing 3 to 6 months of bank statements to prove affordability, you can often access interest rates closer to standard commercial products. This is a brilliant alternative if your credit score is good but not perfect, or if you're a newer business with high turnover. A simple Accountant's Letter can also satisfy many specialist lenders, proving your income without the need for full tax returns. This extra bit of effort can result in significant savings over a five-year loan term.

If an initial no doc application hits a snag, we don't just stop there. We understand the transition from no doc to low doc and can quickly pivot your application by identifying the easiest piece of documentation to provide. This proactive approach ensures your momentum isn't lost, even if a lender asks for a little more clarity on your cash flow.

Maximising Your Approval Odds: The Role of Assets and Credit

Securing no doc business vehicle finance is often less about what you earn and more about what you own. While we've discussed how your ABN and credit history form the foundation of your application, your asset position is the "secret sauce" that many lenders use to finalise an approval. Being asset-backed provides a layer of security that offsets the lack of traditional financial documentation. It signals to the lender that you're an established professional with skin in the game, making you a much lower risk than a business starting from scratch with zero equity.

The vehicle type you select also influences the lender's risk assessment. A brand-new work ute is viewed differently than a ten-year-old specialty van. Lenders look for "resale certainty," meaning they want to know the asset will hold its value if your circumstances change. By choosing a primary business asset and having a clear understanding of your credit standing, you position your business as a reliable partner for commercial lenders.

What Does "Asset-Backed" Actually Mean?

In the eyes of a commercial lender, being asset-backed primarily refers to property ownership. Whether your home is unencumbered or you're still paying off a mortgage, this status drastically improves your approval odds. However, don't be discouraged if you aren't a homeowner yet. Many businesses in the Western Suburbs, from Hoppers Crossing to Melton, successfully gain approval by demonstrating alternative asset strength. This can include equity in an existing fleet of vehicles, ownership of heavy machinery, or even a significant balance in a business savings account. If you're "asset-light," providing a deposit of 10% to 20% can often act as a substitute for property backing, turning a borderline application into a definite approval.

The Importance of the Vehicle as Security

Lenders have a strong preference for utes and vans because they are the workhorses of the Australian economy. These vehicles maintain high demand in the used market, which gives the lender confidence in the security. Age restrictions are a critical factor to watch; most no doc lenders prefer vehicles to be no more than five years old at the start of the loan. A chattel mortgage is the standard commercial security structure where the business takes ownership of the vehicle at the time of purchase while the lender registers a charge over it as security for the loan. This arrangement is the most common path for no doc business vehicle finance because it offers clear tax benefits while protecting the lender's interests. If you're ready to see how your asset position can work in your favour, get a tailored assessment from Quick Choice to explore your specific borrowing capacity.

Streamlining Your Vehicle Finance with Quick Choice

Many business owners reach out to us after being rejected by the "Big Four" banks. Traditional institutions often rely on rigid automated systems that aren't built for the nuances of self-employed life. When the computer says "no" simply because your latest tax returns aren't ready, it doesn't mean your business isn't viable. We specialise in no doc business vehicle finance by looking at the bigger picture. Our role is to bridge the gap between your immediate need for a work vehicle and the flexible commercial lenders who value your ABN and credit history over a stack of paperwork.

The advantage of working with a specialist brokerage like ours is the breadth of choice. Unlike a single bank with one set of rules, we have access to a wide panel of commercial lenders. This variety is crucial because every lender has a different appetite for risk and different criteria for what they consider a "no doc" product. We do the legwork to find the specific lender that fits your asset position and business goals, ensuring you get a competitive deal without the typical bank run-around.

Local Expertise for Western Melbourne Tradies

We are deeply rooted in the Western Suburbs, serving communities from Hoppers Crossing to Tarneit. Our team has watched the rapid growth in Truganina and Rockbank first-hand, and we understand the unique pressures facing transport, construction, and delivery sub-contractors in our region. You aren't just another application number to us; you're a local business owner contributing to our community's expansion. We're committed to fast, supportive communication, ensuring you're never left wondering about the status of your finance while you're out on a job site.

Get Pre-Approved Today

Getting your business moving in 2026 shouldn't be a stressful ordeal. Our process is designed to be as streamlined as the no doc business vehicle finance products we offer. You can check your eligibility without a hard credit hit, which protects your score while we explore your options. All you need to get started is your ABN and a few minutes for a consultation. We'll help you organise your details and identify the best path forward, whether that's a true no doc approval or a low doc alternative that saves you money over the long term.

Don't let administrative hurdles or irregular cash flow cycles slow your momentum. Your business deserves a finance partner that understands the self-employed lifestyle and values your time as much as you do. Organise your no doc vehicle finance with Quick Choice today and secure the gear you need to keep your business growing.

Get Your Business Moving with Confidence

Your business momentum shouldn't be stalled by the administrative weight of traditional lending. We've explored how your ABN longevity and a clean credit history serve as the primary keys to unlocking no doc business vehicle finance. By focusing on your current professional standing and asset position rather than historical tax returns, you can secure the work ute or van you need to keep your contracts on track. Whether you're a property owner or an asset-light contractor in Western Melbourne, there's a tailored finance path available for your specific situation.

As a specialist brokerage dedicated to self-employed Australians, we provide local support and direct access to a panel of over 40 commercial lenders. We understand the unique challenges of the trade and delivery industries in hubs like Tarneit and Hoppers Crossing. You don't have to navigate these complex requirements alone. Speak with a Quick Choice asset finance specialist today to discover a faster, more supportive way to grow your fleet. It's time to put the paperwork aside and get back to what you do best.

Frequently Asked Questions

Can I get no doc vehicle finance with a new ABN?

Lenders typically require your ABN to be active and GST-registered for at least 12 months to qualify for a true no doc product. If your business is younger than a year, you may still secure finance by providing limited bank statements or a larger deposit. This transition into a low doc category allows newer contractors to build their fleet while their business history matures.

Do I need to be a homeowner to qualify for a no doc car loan?

Home ownership is not a mandatory requirement, though it often unlocks lower interest rates and higher borrowing limits. If you're renting or don't own property, you can still qualify by demonstrating a strong credit score or providing a deposit, typically around 20% of the vehicle's value. This "asset-light" approach ensures that established tenants and non-homeowners aren't excluded from the market.

What is the maximum loan amount for no doc business finance?

Most specialist lenders in Australia offer no doc business vehicle finance for amounts ranging from A$10,000 up to A$250,000. The specific limit for your business depends on your credit profile, the type of vehicle being purchased, and whether you have property backing. For amounts exceeding this range, lenders may request some basic proof of income to verify affordability.

How much higher are the interest rates on no doc loans?

Interest rates for no doc products are generally higher than standard commercial loans because the lender accepts more risk by not reviewing your full financials. While a full-documentation loan might start as low as 7.49% p.a., no doc options typically sit at the higher end of the low doc range, which starts between 9.50% and 15% p.a. Your credit score and asset position play the biggest role in determining your final rate.

Can I buy a used vehicle with no doc finance?

Yes, you can finance a used vehicle, provided it meets the lender's age and condition requirements. Most commercial lenders prefer used vehicles to be no more than five to seven years old at the end of the loan term to ensure the asset maintains sufficient resale value. Financing a used ute or van through a private sale may require an independent inspection, whereas dealership sales are often approved faster.

What documents will I actually need to provide for a no doc loan?

You'll primarily need to provide your active ABN, a valid form of identification like a driver's licence, and a signed declaration of income. This declaration confirms that your business can comfortably manage the repayments without needing to show BAS or tax returns. You'll also need to sign a statement confirming the vehicle is for at least 50% business use for tax compliance.

Is a no doc loan the same as a chattel mortgage?

No, these terms refer to different aspects of your finance. "No doc" describes the level of paperwork required to get approved, while a "chattel mortgage" is the legal structure of the loan where you take ownership of the vehicle immediately. Most no doc business vehicle finance applications are structured as chattel mortgages because they offer the most flexibility for GST claims and depreciation for self-employed professionals.

How long does the approval process take with Quick Choice?

Approvals are often secured within 24 to 48 hours once we have your basic details and vehicle choice. Because we bypass the lengthy manual reviews of traditional banks, the digital application process moves quickly. Our goal is to get you a "yes" and have your new work vehicle ready for the road as fast as possible so you don't miss out on upcoming contracts.