Imagine watching a lucrative contract slip through your fingers because your equipment failed and your bank's application process is stuck in slow motion. When you need urgent business asset finance to keep your operations moving, waiting weeks for a "no" isn't just frustrating; it's a genuine threat to your livelihood. You need a solution that respects your time and understands the unique cash flow patterns of a sole trader or contractor in 2026.

It's exhausting to feel like traditional lenders don't speak your language or value your contribution to the economy. We're here to change that narrative by simplifying the path to growth. This guide delivers a fast-track checklist to help you secure approval within 24 to 48 hours using Low Doc options for assets up to $250,000. We'll outline how to organise your ABN, take advantage of the $20,000 instant asset write-off, and position your business for competitive rates without the headache of a full financial audit.

Key Takeaways

- Learn the critical difference between approval and settlement speeds to ensure your equipment is on-site exactly when required.

- Discover the essential document checklist, including ABN age and bank statement requirements, to bypass traditional bank delays.

- Identify why the Low Doc pathway is the most efficient route for securing urgent business asset finance without exhaustive financial reporting.

- Understand the strategic advantage of organising pre-approval before visiting a dealer to strengthen your negotiating position.

- Find out how specialist support for self-employed professionals can streamline the acquisition process for ABN holders across Victoria.

Understanding Urgent Business Asset Finance for Self-Employed Australians

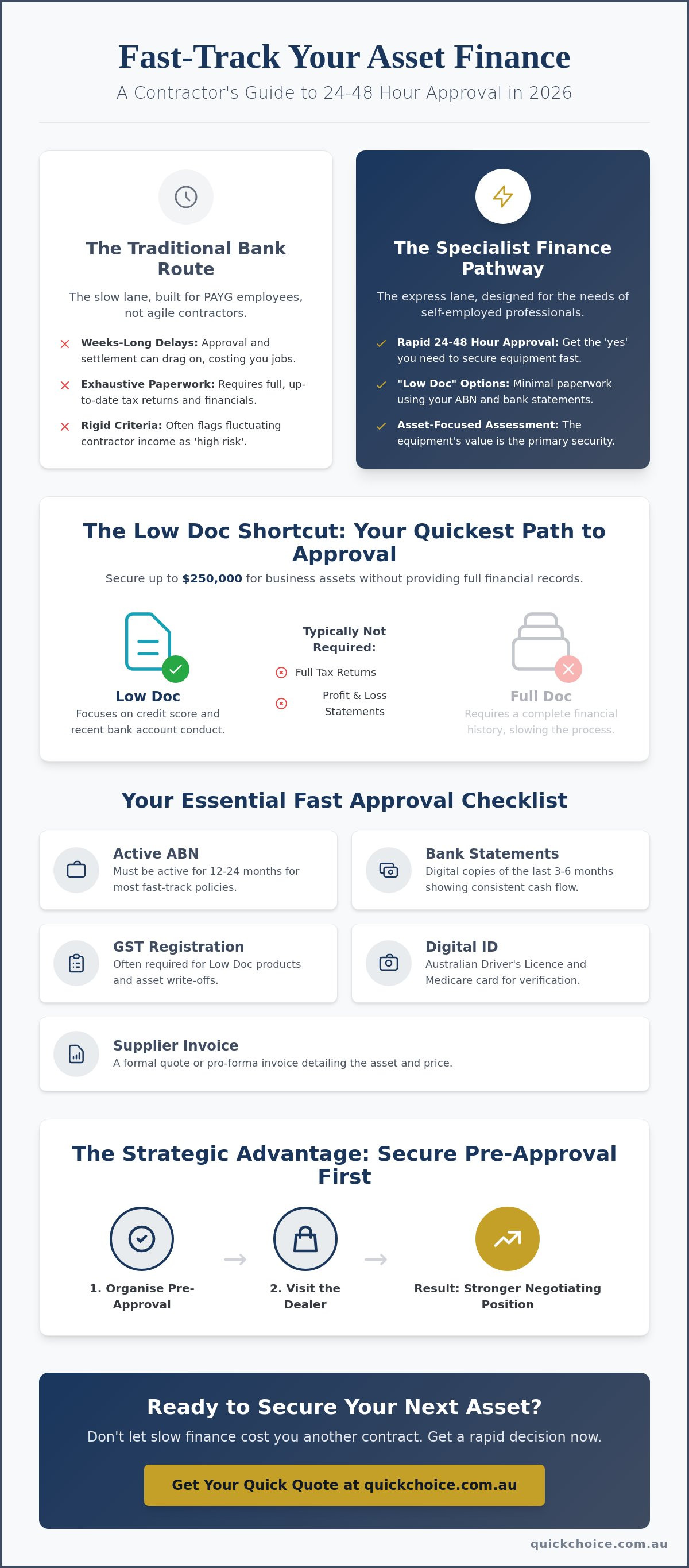

When your business relies on specialised machinery or vehicles, a single mechanical failure can bring your entire operation to a standstill. In these moments, you don't just need a loan; you need urgent business asset finance that moves at the speed of your industry. Speed in this context is measured by two distinct phases: the time to approval and the time to settlement. While many traditional lenders might offer a quick automated response, the actual process of getting funds into a dealer's account can often drag on for weeks. For a sole trader, that delay represents lost revenue and damaged client relationships.

Self-employed professionals frequently encounter roadblocks at major banks because traditional lending models are built for PAYG employees with predictable, static incomes. If your tax returns aren't up to date or your cash flow fluctuates between large contracts, a bank's algorithm may flag you as high risk. Specialist lenders in 2026 have moved away from these rigid constraints. This specialised approach is rooted in Understanding Asset-Based Lending, where the focus shifts from your personal tax history to the inherent value and income-producing potential of the equipment you're purchasing. By utilising "Low Doc" policies, you can often secure approval for assets up to $250,000 with minimal paperwork, provided you have a clean credit history and an active ABN.

When Should You Seek Urgent Finance?

Urgency is usually driven by necessity rather than desire. You might need to replace a core piece of earthmoving equipment that has suffered a terminal breakdown mid-job. Alternatively, you could be a sub-contractor who has just secured a major Victorian infrastructure contract and needs an additional ute or van within the week to start on-site. Rapid finance also allows you to capitalise on time-sensitive opportunities, such as a limited-time stock clearance or a specialised auction where waiting for a standard bank valuation isn't an option.

The Self-Employed Advantage: Niche Lenders vs. Big Banks

Niche lenders understand that a contractor's bank statements often tell a better story than a two-year-old tax return. They prioritse the asset itself as security, which streamlines the assessment process significantly. If you're operating in Melbourne’s western growth corridors like Tarneit or Caroline Springs, working with a specialist who understands the local economic landscape can further accelerate your application. These lenders value the practical reality of your business, recognising that a new asset isn't just a debt; it's the tool that generates your next invoice.

The Essential "Fast Approval" Checklist: Documents You Need Ready

Speed is often a byproduct of organisation. If you are chasing urgent business asset finance, the lender's ability to say "yes" quickly depends entirely on the quality of information you provide upfront. By getting your paperwork ready before you start the application, you eliminate the back-and-forth emails that typically stall the process. Having these items digitalised and ready to upload can mean the difference between a 24-hour approval and a week-long wait.

- Active ABN: Ensure your ABN has been active for the required period, which is usually 12 to 24 months for most fast-track policies.

- Bank Statements: Prepare digital copies of your most recent three to six months of business bank statements to demonstrate consistent cash flow.

- GST Registration: Verify your status, as being GST registered is often a prerequisite for the $20,000 instant asset write-off and certain Low Doc products.

- Digital ID: Have your Australian Drivers Licence and Medicare card ready for the electronic identity verification process.

- Supplier Invoice: Secure a formal quote or pro-forma invoice from your equipment supplier that clearly outlines the asset details and purchase price.

The "Low Doc" Shortcut for Tradies

Low Doc is the primary path for rapid self-employed approval. For a contractor in 2026, this means you don't need to provide full tax returns or profit and loss statements to secure funding. Lenders prioritse your credit score and recent bank account conduct over historical tax data. If your credit file is healthy, you can bypass the heavy paperwork and secure the equipment you need to stay on the tools without delay.

Identity and Compliance Readiness

Modern lenders use digital identity apps to shave hours off the verification process, so ensure your details on the Australian Business Register match your application exactly. Any discrepancy in your business address or structure can trigger a manual review, slowing down your urgent business asset finance request. Maintaining a clean credit file is essential for staying within "auto-approval" limits, which allow systems to process your application without human intervention. You can check your eligibility to see which fast-track options suit your current business structure.

Low Doc vs. Full Doc: Choosing the Quickest Path for Your Business

Deciding between a Low Doc or Full Doc application is the most significant choice you'll make when seeking urgent business asset finance. The primary difference lies in the evidence required to prove your serviceability. Low Doc is the undisputed champion of speed, often delivering a formal approval within 4 to 24 hours. It bypasses the need for intensive financial statements, making it the go-to for busy contractors. Full Doc applications, while potentially offering lower interest rates, require a level of scrutiny that can take several days to clear. If you need a vehicle on the road by Friday, the Low Doc path is almost always the superior strategy.

Interest rates for asset finance in 2026 typically start from approximately 6.25% p.a. for strong-credit businesses. While a Full Doc loan might shave a small percentage off that rate, you must weigh this against the "urgency premium". If waiting for your accountant to finalise last year's tax returns causes you to miss a project start date, the interest savings become irrelevant. For loans under the $250,000 threshold, the efficiency of a Low Doc approval usually outweighs the marginal cost difference.

When Low Doc is the Only Logical Choice

Many self-employed professionals find themselves in a position where their tax returns are not yet finalised. This shouldn't stop you from growing. Modern commercial asset finance policies have evolved to prioritise recent bank conduct over historical data. If you're purchasing a standard asset like a Toyota HiLux or a common piece of earthmoving equipment, lenders are far more likely to grant a rapid approval. The more "liquid" the asset, the faster the process moves.

The Full Doc Alternative: When to Wait a Little Longer

There are times when patience pays off. If you're acquiring large-scale industrial machinery that exceeds the $250,000 Low Doc limit, a Full Doc application is mandatory. This path requires your full financial history, including balance sheets and profit and loss statements. While it takes longer, it allows for bespoke lending structures for complex business needs. Always balance the cost of delay against the potential long-term savings of a slightly more competitive rate.

How to Minimise Delays in Your Asset Finance Application

Securing urgent business asset finance requires more than just a fast lender; it requires a flawless application. Even minor errors can stall a digital approval process, forcing your file into a manual queue for human review. To maintain momentum, you must approach the application with precision. Submitting incomplete or blurry document scans is the most common reason for a delay. Ensure every digit on your bank statements and every word on your identification is crystal clear before hitting send. If a credit analyst cannot read your documents, they cannot approve your loan.

Organising pre-approval before you even step onto a dealership forecourt puts you in the driver's seat. This allows you to act with the same speed as a cash buyer once you find the right equipment. You should also be mindful of "credit hits". Every formal application leaves a footprint on your credit file, and multiple inquiries in a short period can lower your score and signal desperation to lenders. Finally, stay near your phone. Lenders often require a brief verification call to confirm your business details, and missing this call can add an unnecessary 24 hours to your settlement time.

Sourcing the Right Asset for Fast Settlement

The type of asset you choose and who you buy it from significantly impacts your timeline. While approximately 35% of asset finance deals involve private sellers, dealer sales are generally processed faster because the supplier is already a verified entity. Lenders also have "Age of Asset" restrictions. Purchasing brand-new equipment or assets less than five years old usually qualifies for automated "Fast-Track" workflows. If you're looking at older machinery, be prepared for a manual review. Always have the VIN and engine number ready during the initial conversation to ensure the security can be valued immediately.

Leveraging Your Local Broker in Western Melbourne

Working with a specialist who understands the industrial landscape of Truganina, Werribee, or Hoppers Crossing provides a distinct advantage. Local brokers understand the specific cash flow cycles of Melbourne's construction and transport sectors, allowing them to "package" your application to suit the right lender's appetite. A specialist broker acts as a professional filter to ensure your application only reaches lenders whose specific criteria you already meet, effectively preventing unnecessary rejections. If you're ready to move forward, you can get started with an expert who understands the local market and your need for speed.

Partnering with Quick Choice for Rapid Asset Acquisition

Quick Choice isn't just another digital lender with a rigid algorithm. We've built our reputation on being a reliable specialist guide for independent professionals who find themselves underserved by the big banks. While many competitors push you towards automated apps that often reject complex self-employed structures, we prioritse a high-touch, collaborative approach. We understand that when you need urgent business asset finance, you can't afford to be just another ticket in a support queue. Our team combines modern technology with deep niche expertise to ensure your application is seen, understood, and approved without the typical bank red tape.

For ABN holders operating out of growth hubs like Tarneit and Caroline Springs, we provide a streamlined pathway that respects your schedule. We know you're often on the tools or between job sites during standard office hours. Our methodology is designed to fit into your day, moving your request from a pressing need to a settled acquisition in record time. We act as your advocate, ensuring your business's unique cash flow and growth potential are presented in the best possible light to our panel of specialist lenders. This bespoke approach ensures that asset finance for self employed professionals remains accessible even when deadlines are tight.

Why Self-Employed Contractors Choose Quick Choice

Our team possesses a deep understanding of business vehicle finance australia, specifically for the utes and vans that keep local contractors mobile. We maintain access to a curated panel of lenders that specialise in "Fast-Track" approvals, meaning we know exactly which door to knock on to get your result. By handling the heavy lifting of the documentation process, we relieve the stress of paperwork. This allows you to stay focused on your job site while we secure the tools you need to finish the project and grow your business.

Get Started with Your Urgent Application Today

Taking the first step is straightforward. Your journey begins with a focused 15-minute consultation where we assess your requirements and identify the most efficient lending path for your urgent business asset finance request. We pride ourselves on absolute transparency regarding rates and fees, ensuring you have all the facts before making a commitment. There are no hidden surprises or abstract promises; we provide practical results delivered with professional warmth. Organise your urgent business asset finance with Quick Choice today and experience a partnership built on your success.

Take Control of Your Business Growth Today

Securing the equipment you need shouldn't be a battle against red tape. By following the fast-track checklist and prioritising your digital documentation, you've already cleared the biggest hurdles to success. Remember that Low Doc options are your most efficient tool for acquisitions up to $250,000, especially when your tax returns aren't quite ready for a bank's scrutiny.

When you need urgent business asset finance, the difference between a missed opportunity and a new contract often comes down to the specialist you choose. As a dedicated self-employed broker serving Truganina and Western Melbourne, we focus on removing the obstacles that slow you down. We're here to ensure your application is packaged correctly from the start, giving you the best chance at a rapid approval through our fast-track Low Doc options.

Don't let a terminal breakdown or a sudden contract opportunity stall your momentum. We're ready to help you bridge the gap between where you are and where you want to be. Get a Fast-Track Asset Finance Quote Now

Your next big project is waiting, and we're here to help you gear up for it with confidence.

Frequently Asked Questions

How fast can I realistically get business asset finance approved?

You can realistically receive an approval for urgent business asset finance within 4 to 24 hours for standard assets like utes, vans, or common machinery. This rapid turnaround depends on having your digital documents ready for immediate upload. While the approval itself is fast, the final settlement usually occurs once the lender verifies the supplier's invoice and your identification.

Can I get urgent finance if I have a new ABN?

Yes, you can secure finance with a newer ABN, provided you've been trading for at least six months. Many specialist lenders prioritse your recent bank conduct and industry experience over the total age of your business. Some lenders even report high approval rates for businesses that have been operating for less than two years, as long as cash flow is consistent.

What is the maximum amount I can borrow under a Low Doc policy?

The standard threshold for Low Doc asset finance is up to $250,000 for eligible self-employed applicants. This limit allows you to bypass the need for full tax returns or formal profit and loss statements. If your equipment needs exceed this amount, you'll typically need to move to a Full Doc application, which requires more comprehensive financial history.

Will applying for urgent finance hurt my credit score?

A single application for urgent business asset finance leaves a standard inquiry on your credit report, which typically has a negligible effect. The risk arises if you submit multiple applications to different lenders in a short window, as this can signal financial distress and lower your score. It's wiser to use a broker to target the most likely lender first.

Do I need to provide a deposit for urgent equipment finance?

You can often secure 100% finance with no upfront deposit because the asset you're purchasing acts as the primary security for the loan. This is a common feature for self-employed professionals who want to keep their cash in the business. Some lenders might only request a deposit if the equipment is highly specialised or has a limited resale market.

Is urgent finance available for used vehicles and machinery?

Urgent finance is available for used assets, though the age of the equipment can change the approval pathway. Assets under five years old usually qualify for automated "fast-track" systems that deliver decisions in hours. For older machinery, the lender might require a manual assessment or a private sale inspection, which can add a day to the process.

What happens if my application is declined by a major bank?

A rejection from a major bank isn't the end of the road; it often just means you didn't fit their rigid, automated criteria. Specialist lenders are far more flexible and focus on your business's recent cash flow and the asset's value. They're often more willing to work with contractors who have fluctuating seasonal incomes or newer business structures.

Are there specific tax benefits for urgent asset purchases in 2026?

Small businesses with an aggregated turnover of less than $10 million can access the $20,000 instant asset write-off for the 2025-2026 financial year. This applies to eligible assets first used or installed ready for use by June 30, 2026. It's an effective way to improve your cash flow by immediately deducting the cost of essential business tools from your taxable income.