Does the thought of compiling years of tax returns feel more daunting than the actual work you do on-site? You aren't alone; many local tradies and business owners find that proving self employed income for a loan Tarneit is often the most stressful part of expanding their operations. Since APRA limited high debt-to-income lending to just 20% of new loans in February 2026, the traditional bank application process has only become more rigid. It's understandable if you're worried that a fluctuating bank balance or a late BAS might stand between you and the equipment you need to grow.

We're here to change that narrative by showing you a more streamlined path to success. You'll learn exactly how to verify your earnings for asset and equipment finance without the usual paperwork headaches or fear of rejection. This guide explains the critical differences between Low Doc and Full Doc loans in the current 2026 financial climate; where the RBA cash rate sits at 4.35%. We also provide a practical checklist of required documents so you can secure fast approval for your next work vehicle or machinery with confidence.

Key Takeaways

- Distinguish between Full Doc and Low Doc pathways to determine the most efficient route for your specific business structure.

- Learn why proving self employed income for a loan Tarneit is often faster using Business Activity Statements (BAS) or bank statements rather than waiting for annual tax returns.

- Identify the essential 2026 documentation required to secure asset finance for work vehicles and machinery without administrative delays.

- Discover how the "Equity Factor" and a clean credit file can offset seasonal income fluctuations and strengthen your application.

- Understand how partnering with a specialist finance broker provides access to a broader panel of lenders tailored to the needs of local tradies and business owners.

Navigating Income Evidence for Self-Employed Loans in Tarneit

Running a business in Tarneit's booming construction or transport sectors is a significant achievement. However, when you need a new ute or heavy machinery to keep up with local demand, the income verification process often feels like a brick wall. Lenders view self-employed income through a different lens than a standard PAYG salary. Your earnings don't arrive in neat, predictable packets; they reflect the ebb and flow of your contracts. This inherent complexity is why proving self employed income for a loan Tarneit requires a specialist approach that looks beyond a simple payslip.

Tarneit is expanding rapidly, with 2021 census data showing that transport and construction are among the top industries for local workers. For these professionals, asset finance often provides a more flexible path than a standard home loan. While residential mortgages are now subject to the strict APRA debt-to-income limits introduced in February 2026, equipment and vehicle finance focus heavily on the utility of the asset itself. A specialist broker acts as your translator here. We take your business success and turn it into the data-driven evidence that lenders demand.

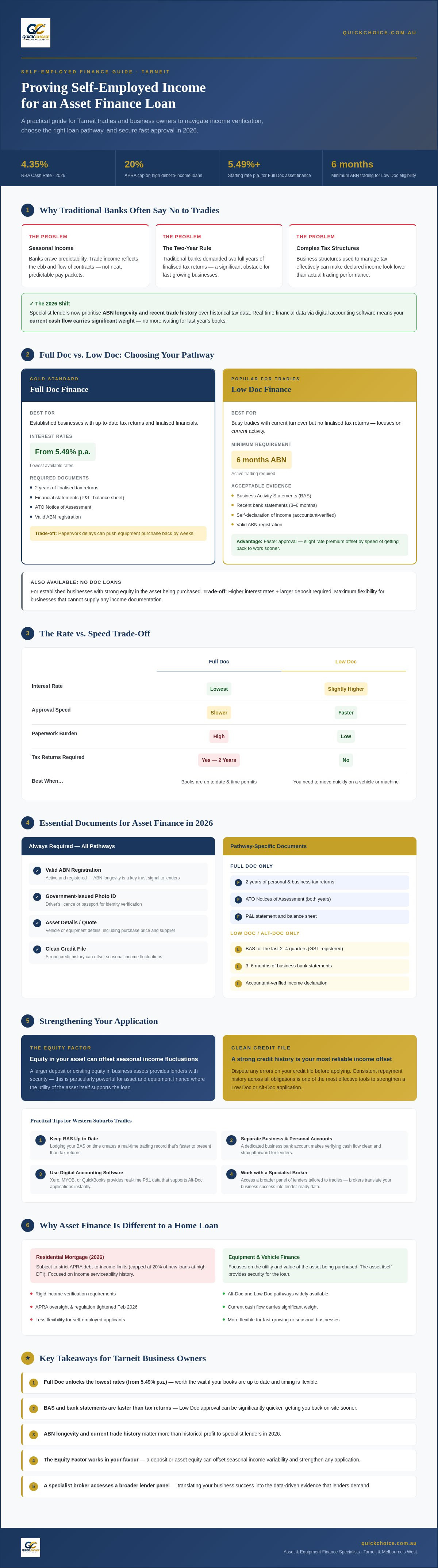

Why Traditional Banks Often Say No to Tradies

Traditional lenders crave predictability. They often struggle with the seasonal nature of trade work or the tax structures that business owners use to manage their finances. For decades, the "Two-Year Rule" was an immovable obstacle, requiring two full years of finalised tax returns before a bank would consider an application. In 2026, this is no longer the only way to secure funding. Many specialist lenders now prioritise your ABN longevity and recent trade history over historical tax data. This shift is vital for businesses that have scaled quickly or invested heavily back into their operations recently.

The 2026 Shift: Real-Time Financial Data

Modern finance is built on speed and accuracy. Digital accounting software has completely changed how we handle the verification process. Instead of waiting for your accountant to finish last year's books, we can often use real-time data to demonstrate your business health. This "Alternative Documentation" (Alt-Doc) approach means your current turnover and recent bank statements carry significant weight. Lenders are increasingly interested in your current cash flow rather than a profit and loss statement from eighteen months ago. It's a more logical way to assess a growing business in a fast-paced market like Melbourne's west.

Full Doc vs. Low Doc: Choosing Your Pathway

Deciding how to present your financial health to a lender is the most critical step in your application. For many business owners in Melbourne's west, the choice between Full Doc and Low Doc depends entirely on whether you have met the official record-keeping requirements for the current financial year. While a Full Doc loan offers the most competitive interest rates, it requires a level of paperwork that many busy tradies haven't finalised yet. Understanding these pathways ensures you don't waste time on an application that doesn't fit your current situation.

Low Doc loans have become a popular alternative for those proving self employed income for a loan Tarneit because they focus on current turnover rather than historical profit. If you've been trading for at least six months and have a valid ABN, you can often bypass the need for full tax returns by providing Business Activity Statements (BAS) or bank statements. In rarer cases, a "No Doc" loan might be an option if the asset you're purchasing provides enough security for the lender. These typically carry higher interest rates and require a larger deposit, but they offer the ultimate in flexibility for established businesses with strong equity.

Comparing these levels of documentation is about balancing cost against convenience. Full Doc remains the cheapest way to borrow, but the "paperwork headache" can delay your equipment purchase by weeks. If you need to move quickly on a piece of machinery or a new vehicle, the slightly higher rate of a Low Doc loan is often offset by the speed of approval and the ability to get back to work sooner. If you are feeling overwhelmed by the choices, speaking with a specialist guide can help clarify which path suits your specific trade.

When to Choose Full Doc Finance

If your business is established and your tax returns are up to date, Full Doc is the gold standard. It unlocks the lowest interest rates, which were seen starting from 5.49% p.a. for asset finance in July 2026. You'll need to provide two years of personal and business tax returns along with your ATO notices of assessment. This path is best for established businesses with stable, long-term growth that want to maximise their borrowing limits for significant capital investments.

The Advantages of Low Doc for Contractors

Speed and simplicity are the primary drivers for Low Doc finance. It allows for rapid approvals without waiting for your accountant to finalise your year-end books, which is a common pain point for sub-contractors with varying monthly invoices. This is particularly relevant for local owner-drivers who need self employed truck finance to secure their next contract. By using 6 to 12 months of trade history, you can demonstrate a clear picture of your turnover and secure the funds you need to keep your business moving forward.

Essential Documents for Asset Finance in 2026

Gathering documents doesn't have to be a chore. When proving self employed income for a loan Tarneit, focus on the "Big Three": Business Activity Statements (BAS), bank statements, and your identity credentials. Lenders in 2026 use these to verify that your business isn't just surviving, but thriving enough to support new debt. Unlike personal loans, asset finance is designed to be efficient; the documents required are often those you already use to manage your daily operations.

Your ABN is more than just a number; it's a record of your business's longevity. Lenders often look for a minimum of 12 to 24 months of active trading history, though some specialist asset lenders are more flexible. Verifying your GST status is equally important, particularly if you're looking to finance a commercial vehicle. If your registration isn't up to date, it can trigger a manual review that slows everything down. A quick check on the ABN Lookup tool before you start can save you hours of back-and-forth later.

Proving Income with BAS and Bank Statements

Lenders typically request the last two quarters of BAS or 6 to 12 months of business bank statements. They look for consistent credits that align with your declared turnover. Healthy closing balances and a lack of overdrawn fees are vital indicators of financial stability. It's also wise to avoid mixing personal expenses with your business account. When a lender sees your grocery bill or gym membership coming out of the same account as your trade supplies, it clouds their view of your true business expenses. Keeping a dedicated business account ensures that when you use equipment finance for sole traders, the lender sees a clear, profitable operation.

The Role of the Accountant’s Letter

If your tax returns aren't ready, an accountant’s letter is a powerful tool. This professional declaration confirms your taxable income and business solvency. In 2026, a valid letter must clearly state your business name, ABN, and a specific income figure for the most recent financial year. Lenders trust these declarations because they are backed by your accountant's professional liability. It's a high-trust document that can bridge the gap between your real-world success and the lender's data requirements. Just ensure the figures in the letter match the "Financial Position" you've declared on your application to avoid any confusion. This consistency shows the lender that you have a firm grip on your numbers.

Strengthening Your Application: Tips for Western Suburbs Tradies

Securing finance in a fast-growing hub like Tarneit requires more than just showing a healthy bank balance. You need to present a narrative of stability and purpose to the lender. While proving self employed income for a loan Tarneit is the foundation of your file, several other factors can influence your interest rate and approval speed. Lenders in 2026 are particularly focused on the quality of your credit history. Even a small, forgotten utility default from years ago can signal risk in a tighter lending environment. We recommend checking your credit report before applying to ensure every detail is accurate and up to date.

The "Equity Factor" is another powerful tool at your disposal. If you're finding it difficult to provide extensive documentation, a larger upfront deposit can often bridge the gap. By putting down 10% or 20% toward the asset, you reduce the lender's risk significantly. This often leads to more flexible income verification requirements and can even unlock more competitive rates. For those in earthmoving or transport, clearly defining the "Business Purpose" of the asset is essential. Lenders want to see how a new excavator or prime mover will directly increase your turnover or reduce your operational costs.

Local Insights for Tarneit and Melton Contractors

Local contractors in the Western Suburbs are currently benefiting from a massive pipeline of infrastructure and residential projects. If you have signed contracts for upcoming work in Melton or new estates in Tarneit, include these in your application. Showing a guaranteed future income stream provides immense confidence to a credit assessor. Many business owners in nearby Hoppers Crossing and Werribee are increasingly turning to commercial asset finance to scale their fleets quickly. Ensure your ABN has been active for the required period and your GST registration is current, as these are non-negotiable minimums for most specialist lenders.

Avoiding Common Application Mistakes

One of the most frequent errors we see is "over-declaring" income. It's tempting to state your gross turnover as your net income, but lenders will quickly cross-reference your claims against your bank credits. If the numbers don't align, it creates a red flag that can be hard to overcome. Additionally, avoid making multiple credit enquiries in a short window. Every time you "shop around" and a lender runs a hard credit check, it leaves a mark on your file. This can make you appear desperate for credit, even if you're just doing your due diligence. If you want to explore your options without damaging your credit score, you should get a personalised quote from a specialist who understands the local market.

Finally, ensure your asset choice aligns with your business size. A sole trader courier applying for a fleet of five vans without a clear expansion plan may face extra scrutiny. By keeping your application realistic and backed by the local insights we've discussed, proving self employed income for a loan Tarneit becomes a much smoother, more predictable process.

How Quick Choice Simplifies Finance for Tarneit Business Owners

We understand that the paperwork side of business is rarely the reason you started your trade. While proving self employed income for a loan Tarneit can feel like an uphill battle at a major bank, we specialise in making the complex feel straightforward. Our team doesn't just look at a balance sheet; we look at the potential of your business. By acting as your local guide, we translate your hard work into a format that lenders respect and reward.

Our expertise is backed by a panel of over 40 lenders, ranging from the big four banks to boutique specialists that focus exclusively on asset finance for self employed professionals. This broad access means we don't have to force your business into a "one size fits all" box. Whether you're based in Truganina or right in the heart of Tarneit, we provide a high-touch service that respects your time and your ambition. We take pride in being a collaborator for local businesses, helping you navigate the 2026 lending environment with quiet confidence.

Our Process: From Enquiry to Delivery

We follow a methodical three-step approach to get you the machinery or vehicle you need. First, we conduct a thorough assessment of your business goals and current documentation to see where you stand. We don't just ask for papers; we help you understand what they say about your business health. Next, we handle the lender matching process, identifying the specific Low Doc or Full Doc pathway that offers you the best terms. Finally, we manage the settlement process from start to finish. Our goal is to get you operating your new equipment sooner, ensuring your business momentum never stalls due to finance delays.

Start Your Application Today

Don't let the fear of a complex application hold your business back. We offer no-obligation consultations for local Western Suburbs business owners who need clear, expert guidance on their next move. Whether you're ready to apply or just need to understand how to prepare your file, we're here to help. Our team provides the niche expertise you need to overcome any documentation obstacles. Contact the Quick Choice team for a tailored quote and take the first step toward securing the future of your business today.

Empowering Your Business Growth in Melbourne's West

Securing the right machinery or vehicle is about more than just a transaction; it's about the momentum of your business. We've explored how the 2026 lending landscape rewards those who present their financial story clearly. Whether you choose the path of a Full Doc application or leverage the speed of a Low Doc solution using your BAS, success lies in the details. By maintaining a clean credit file and understanding the "Equity Factor", you position your business as a reliable partner for lenders.

The process of proving self employed income for a loan Tarneit is significantly smoother when you have a specialist guide by your side. Since 2017, we've served sole traders and contractors across Tarneit, Truganina, and the broader Western Suburbs. We take pride in our ability to find Low Doc and No Doc solutions that big banks often overlook. Your ambition deserves a finance partner that speaks your language and values your time.

Ready to take the next step? Get a specialist asset finance quote for your Tarneit business today. We look forward to helping you drive your business forward with confidence.

Frequently Asked Questions

Can I get a loan in Tarneit if I’ve only been self-employed for 6 months?

Yes, you can. While many major banks prefer a two-year trading history, certain specialist lenders offer pathways for businesses with a six-month ABN registration. This is particularly common if you have significant prior experience in the same industry. You'll likely need to provide bank statements to show consistent turnover during those initial months to secure approval.

Do I need to provide my house as security for a self-employed equipment loan?

No, you typically don't need to use your home as collateral. Asset finance is designed so that the vehicle or machinery you're purchasing acts as the primary security for the lender. This keeps your personal assets separate from your business debt. It's a safer way for local contractors to grow their fleet without putting the family home at risk.

What is the minimum ABN registration period for a Low Doc loan in 2026?

Most Low Doc lenders in 2026 require a minimum of six months of active ABN registration. However, having an ABN that's been active for over 12 or 24 months often unlocks more competitive interest rates. Lenders use your ABN history as a measure of business stability; the longer you've been trading, the stronger your application becomes.

How much income do I need to show for a $50,000 work ute?

Lenders focus on your "serviceability" rather than a single, fixed income figure. For a $50,000 work ute, they'll check that your business turnover comfortably covers the monthly repayments after all other expenses are paid. When proving self employed income for a loan Tarneit, showing consistent monthly credits on your bank statements is more important than having a massive end-of-year profit.

Can I use my BAS to prove income if I haven’t filed my tax return?

Yes, using your Business Activity Statements (BAS) is the standard method for Low Doc applications. If your latest tax returns aren't finalised, providing the last two to four quarters of BAS allows lenders to verify your recent turnover. This real-time data is often more reflective of your current business health than a tax return from the previous financial year.

Will a "Bad Credit" history stop me from getting asset finance?

A less-than-perfect credit history doesn't have to be a deal-breaker. While a "Bad Credit" history might lead to a higher interest rate, many specialist asset lenders look at the context of your business performance. If you can show strong recent turnover and a clear business purpose for the asset, we can often find a pathway to approval that traditional banks would reject.

What is a "Declaration of Financial Position" and do I need one?

A Declaration of Financial Position is a document where you self-certify your assets and liabilities. You'll likely need one for a Low Doc loan application. It provides a snapshot of what you own and what you owe, helping the lender understand your overall financial strength. It's a straightforward form that we can help you complete accurately to ensure your file is lender-ready.

How long does it take to get a self-employed loan approved in the Western Suburbs?

Approval times are often remarkably fast for self-employed professionals. For a Low Doc application with all the correct paperwork, you can frequently see an approval within 24 to 48 hours. This streamlined process is designed to help Tarneit business owners move quickly when a new contract starts or a piece of equipment needs urgent replacement.