Using your own hard-earned cash to buy new equipment might actually be the most expensive way to grow your business in 2026. With the RBA increasing the official cash rate in May, the choice between asset finance vs business loan has become a pivotal decision for every self-employed Australian looking to stay competitive. You likely feel the pressure of rising operational costs and the constant worry that a complex application process will lead to another "no" from a traditional bank.

We agree that your focus should be on winning bigger contracts, not drowning in paperwork or risking your family home to secure a simple piece of machinery. This article promises to help you identify the most cost-effective funding path to preserve your cash flow and keep your personal assets protected. We will compare current interest rate trends, explain how to leverage the $20,000 instant asset write-off, and show you which option offers the best tax advantages for your ABN venture this year.

Key Takeaways

- Learn how to choose between asset finance vs business loan by evaluating whether you need to secure a specific piece of equipment or fund broader operational growth.

- Discover how "Low Doc" application paths allow ABN holders to bypass the complex paperwork of traditional banks and secure gear faster.

- Understand the security advantages of asset finance, which typically uses the equipment itself as collateral to help protect your personal wealth.

- Maximise your 2026 cash flow by leveraging GST input tax credits and the $20,000 instant asset write-off for eligible business purchases.

- Master a simple "Rule of Thumb" checklist to determine which funding path matches your immediate contract needs and long-term business goals.

Navigating the Choice: Asset Finance vs Business Loan for Self-Employed Australians

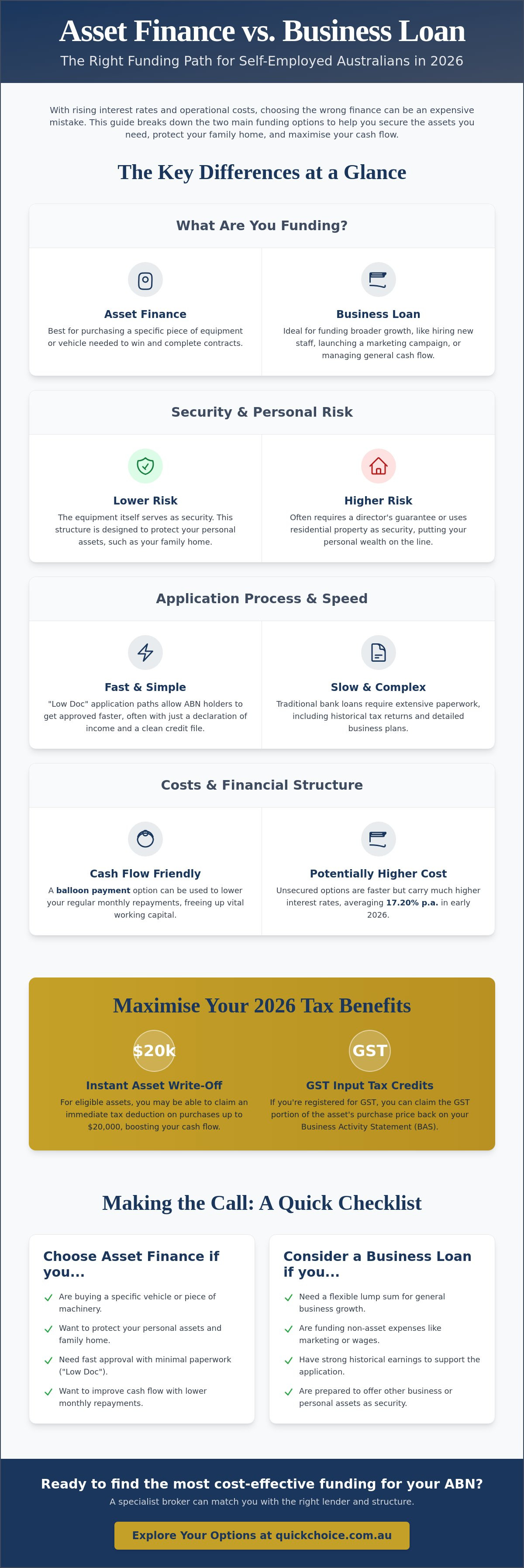

Choosing between asset finance vs business loan is one of the most significant financial crossroads you'll face as a self-employed professional in 2026. The Australian lending market shifted significantly in May 2026 when the RBA increased the official cash rate, prompting major banks to lift their variable business rates. This change means the cost of choosing the wrong structure is higher than ever. While a big bank might offer a generic product, these "one size fits all" solutions often fail contractors because they don't account for the unique, often seasonal cash flow cycles of an ABN holder.

Specialist lenders have stepped into this gap, offering more bespoke options for the 97.2% of Australian businesses that are classified as small enterprises. The decision usually comes down to what you are actually buying. If you're purchasing a specific piece of equipment to help you take on a bigger contract, asset finance is designed for that exact purpose. If you need a flexible pool of cash to cover general expenses, a business loan might be the better fit.

What Exactly is Asset Finance?

Asset finance is a targeted funding solution where the equipment or vehicle you're buying serves as the primary security for the debt. This structure is a game-changer for self-employed Australians because it frequently allows for "Low Doc" applications. Instead of providing years of historical tax returns, you can often secure funding based on your current ABN status and credit profile. Common structures include chattel mortgages and hire purchases, which allow you to own or use the asset while preserving your other borrowing capacity. By using the equipment as collateral, you avoid the need to put up your family home as security, keeping your personal wealth protected if the business hits a snag.

The Fundamentals of a Business Loan

A business loan provides a lump sum of capital for broader purposes that aren't tied to a specific piece of hardware. You might use these funds to hire a new team, launch a marketing campaign, or manage the transition to the new "Payday Super" requirements starting in July 2026. Reviewing Business loan basics helps clarify that these can be secured by residential property or remain unsecured. Unsecured options are faster to access but carry higher interest rates, which reached averages of 17.20% p.a. in early 2026. Banks typically use a "cash flow" lending model here, looking closely at your business's overall goodwill and historical earnings to determine your limit.

Success depends on matching the finance term to the useful life of the asset. You don't want a seven-year loan for a piece of technology that will be obsolete in three. A specialist broker acts as your guide through this process, helping you bypass rigid corporate banking models. They understand that an ABN holder in 2026 needs flexibility and speed to secure the equipment required for growth without getting bogged down in unnecessary red tape.

Understanding Asset Finance: Securing Equipment for Growth

Asset finance moves at a pace that traditional business loans simply cannot match. For a self-employed professional in Melbourne, waiting weeks for a bank's credit committee to review a mountain of paperwork isn't just frustrating; it's a lost opportunity. When comparing asset finance vs business loan options, the speed of "Low Doc" approvals stands out as a primary advantage. These pathways often allow ABN holders to secure funding for essential gear based on a simple declaration of income and a clean credit history, rather than exhaustive historical financial statements.

The security structure of this funding provides a significant layer of protection for your personal wealth. In this model, the lender uses the equipment itself as collateral. If your business faces a sudden downturn, the lender's claim is generally limited to that specific asset. This is a far more reassuring path than a standard business loan, which might require a director's guarantee or a mortgage over your family home. You maintain your peace of mind while gaining the tools needed to scale your operations.

To keep monthly commitments manageable, many contractors opt for a balloon payment at the end of the term. This structure reduces your regular repayments, freeing up cash to cover other operational costs like the new "Payday Super" obligations or rising fuel prices. If you're ready to see how these structures fit your specific trade, exploring Asset Finance for Self Employed options can provide the clarity you need to move forward.

Common Structures: Chattel Mortgage vs Leasing

Most Australian tradies prefer a chattel mortgage because it allows them to claim the GST on the purchase price in their next Business Activity Statement (BAS). This provides an immediate cash flow injection that can be vital for growing ventures. Leasing is often a better fit for technology or high-turnover assets where you want to upgrade frequently without the burden of ownership. Understanding how does asset finance work simplifies the acquisition process for contractors, ensuring you don't get bogged down in technical jargon. You can also research broader Australian government funding options to see how these structures align with current tax incentives like the $20,000 instant asset write-off.

Why Self-Employed Professionals Prefer Asset-Backed Funding

The ability to upgrade equipment frequently is essential to staying competitive in 2026. For businesses in Truganina and Werribee that rely on heavy machinery or specialized transport, having the latest gear means less downtime and lower maintenance costs. Asset-backed funding supports this cycle by making it easier to trade in old equipment and roll the remaining balance into a new agreement. It's a streamlined approach that values your time as much as your talent, allowing you to focus on the job at hand rather than the fine print of a bank's lending criteria.

The Role of Business Loans: Flexibility Beyond Physical Assets

While asset finance is the go-to for securing hardware, a business loan serves a different purpose entirely. It provides the capital needed for intangible growth or operational hurdles that don't come with a serial number. If you are looking to acquire a competitor's client list or fund a major rebranding project, a business loan is often your only logical path. When weighing up asset finance vs business loan options, remember that a loan funds your vision, whereas finance secures your tools.

You generally choose between two main structures: a term loan or a line of credit. A term loan delivers a lump sum upfront, which you repay over a fixed period. This is ideal for one-off investments with a clear "Return on Investment" plan. Conversely, a line of credit acts as a financial safety net. You only pay interest on the funds you actually use, making it a popular choice for managing the cash flow gaps created by the ATO's increased scrutiny on GST and payroll in 2026. Consult the Australian government guide to business funding to see how these broader products compare to specific equipment-based finance.

Unsecured Business Loans: Speed at a Cost

Modern Australian fintech lenders have revolutionised access to capital, often providing a decision within a 24 to 48 hour window. This speed is incredibly valuable when you need to jump on a bulk stock discount or handle emergency repairs to keep a project moving. However, this convenience comes with a warning. Because these loans lack physical collateral, interest rates are significantly higher. In early 2026, average rates for unsecured business loans reached approximately 17.20% p.a. Using this high-interest debt for long-term equipment purchases is usually a mistake that can quickly erode your profit margins.

Secured Business Loans: Lower Rates, Higher Risk

If you need a lower interest rate, a secured business loan requires you to provide collateral, typically residential or commercial property. While this reduces the lender's risk and your monthly interest cost, it places your most valuable personal assets on the line. This structure can also hinder your ability to refinance your home or access equity for personal use later. Specialists often suggest avoiding this path for equipment purchases. Why risk your family home for a new excavator when asset finance allows the machine to secure its own debt? It's about choosing the right level of risk for the specific reward you're chasing.

Key Differences: Security, Interest Rates, and Tax Implications

The financial gap between asset finance vs business loan options often comes down to the lender's perception of risk. Because asset finance is secured by the equipment itself, interest rates typically start from approximately 7.49% p.a. in the current 2026 market. Compare this to unsecured business loans, where interest rates can climb to an average of 17.20% p.a. because the lender has no physical collateral to claim if things go wrong. Choosing the asset-backed path doesn't just lower your monthly commitment; it signals to lenders that you're making a calculated, low-risk investment in your own productivity.

Your balance sheet also reacts differently to these structures. A specific equipment finance agreement is often seen as "good debt" by future lenders because it's tied to a revenue-generating tool. This can preserve your overall borrowing power for when you eventually want to expand your premises or seek a larger line of credit for working capital. It's about maintaining a clean separation between the debt that grows your business and the debt that sustains it.

The Security Factor: Protecting the Family Home

Many self-employed Australians fall into the trap of signing a General Security Agreement (GSA) for a standard business loan. This "all-presents-and-future-assets" clause gives the lender a claim over almost everything the business owns, and often requires a personal guarantee. Asset finance is different because the security is usually limited to the specific machine or vehicle you are purchasing. Keeping your business and personal debt separate is the most effective way to ensure a business hiccup doesn't threaten your family home. For a deeper look at these safeguards, you can read about asset finance without property security to understand how to ring-fence your personal wealth.

Tax and Cash Flow: The Bottom Line

The 2026 tax landscape offers significant incentives for ABN holders who choose the right structure. Under a chattel mortgage, you can generally claim the full 10% GST on the purchase price in your next BAS, providing an immediate cash injection. You also benefit from the $20,000 instant asset write-off threshold if your business turnover is under $10 million. A business loan doesn't offer the same GST advantages, as the loan principal itself isn't a taxable supply. Understanding mistakes to avoid when financing equipment often stems from choosing the wrong tax structure for your specific turnover level.

If you want to secure the gear you need while keeping your tax obligations optimised, our team can help you find the right fit. Explore our Asset Finance for Self Employed solutions to see how we can support your growth in 2026.

Making the Call: Which Funding Path Matches Your 2026 Goals?

Deciding between asset finance vs business loan often boils down to a simple rule of thumb: are you buying "stuff" or "time"? If your goal is to acquire a physical tool that generates income, asset-backed funding is almost always the more cost-effective choice. If you need capital to bridge a gap, hire staff, or fund a marketing push, a business loan provides the flexibility that equipment finance cannot. In the 2026 Australian economy, where efficiency is paramount, matching your funding to your objective is the smartest way to protect your margins.

Consider these local scenarios to see where your business fits:

- Scenario A: An earthmoving contractor in Melton needs a new excavator to start a major civil works project. Asset finance is the ideal fit, allowing the machine to secure the debt while keeping interest rates low and protecting personal property.

- Scenario B: A courier business in Hoppers Crossing wants to add three new vans to their fleet. By using asset finance, they can leverage the $20,000 instant asset write-off for each eligible vehicle while preserving their cash reserves for fuel and maintenance.

- Scenario C: A consultant in Caroline Springs needs a cash injection to develop a proprietary software tool and hire a virtual assistant. A business loan is the logical path here, as there is no physical asset to act as collateral for the lender.

Industry-Specific Recommendations

In the transport and logistics sector, specialized truck finance usually outperforms a general business loan. Lenders in this space understand the resale value of heavy vehicles, which leads to more competitive terms and higher approval chances for ABN holders. For construction and tradies, using the asset as security is the most reliable way to bypass the need for residential property collateral. Professional services, however, often rely on business loans to fund "intangibles" like intellectual property or market expansion, where the return on investment is measured in future billable hours rather than machine uptime.

Next Steps: How to Organise Your Application

Getting your paperwork in order is the first step toward a successful funding outcome. You'll generally need your current ABN details, the last six months of business bank statements, and a formal quote for the asset you intend to purchase. Working with a specialist broker like Quick Choice helps you navigate these options without the stress of "credit shopping" at multiple banks. We understand the unique needs of self-employed Australians and can help you secure the right structure before your next big contract starts. For a more detailed roadmap, check out our ultimate 2026 Australian guide to ensure your venture is positioned for long-term success.

Empower Your ABN Venture with Smarter Funding

Choosing between asset finance vs business loan doesn't have to be a source of stress for your self-employed journey. You now understand that while a business loan offers essential flexibility for general growth, asset finance provides a safer and more cost-effective way to secure the tools of your trade. By using the equipment as its own security, you protect your family home and keep your personal wealth ring-fenced from business risks. You also position your venture to take full advantage of 2026 tax incentives like the $20,000 instant asset write-off.

Since 2017, we've acted as specialist guides for contractors and small business owners across Truganina, Werribee, and the surrounding western suburbs. Our innovative Low Doc solutions mean you spend less time on paperwork and more time winning new contracts. If you're ready to see how the right structure can transform your cash flow and protect your future, Get a Tailored Asset Finance Quote from Quick Choice today. We're here to help you build a more resilient and profitable business.

Frequently Asked Questions

Is it easier to get asset finance or a business loan as a sole trader?

Asset finance is typically much easier for a sole trader to secure than a standard business loan. Because the equipment or vehicle serves as its own security, lenders face less risk and often offer "Low Doc" application paths. You won't always need years of tax returns to prove your income. This makes it a faster, more accessible choice for ABN holders who need to upgrade their gear quickly to stay competitive.

Can I get asset finance without providing my house as security?

Yes, you can definitely secure asset finance without using your family home as collateral. The lender uses the specific asset you're purchasing as the primary security for the debt. This keeps your personal property separate from your business obligations. If your venture hits a rough patch, your home remains protected, which is a significant advantage when comparing asset finance vs business loan structures that might require a property-backed guarantee.

What are the current interest rate differences between the two in 2026?

In May 2026, interest rates for asset finance vs business loan options vary significantly based on security. Asset finance interest rates generally start from approximately 7.49% p.a. for well-qualified applicants. Secured business loans also start around this mark; however, unsecured business loans are much more expensive. Following the RBA cash rate hike, average rates for unsecured lending have climbed to around 17.20% p.a., making asset-backed debt a far more cost-effective path.

How does the GST claim work for asset finance vs a business loan?

If you use a chattel mortgage structure for your asset finance, you can usually claim the full 10% GST on the purchase price in your next Business Activity Statement. This provides an immediate boost to your cash flow. A standard business loan doesn't offer this benefit because the loan principal itself isn't a taxable supply. You should always confirm your eligibility with an accountant based on your current GST registration status.

Do I need a new ABN to qualify for equipment finance?

You don't need a new ABN; in fact, having an established ABN is usually a requirement for the best rates. Most specialist lenders look for an ABN that's been active and GST-registered for at least two years to qualify for "Low Doc" finance. If your ABN is newer than that, you might still find options, but you'll likely need to provide more detailed financial evidence to support your application and prove your business's viability.

What happens if I can’t make the payments on my asset finance?

If you fall behind on your asset finance payments, the lender has the right to repossess the specific equipment or vehicle used as security. They will typically sell the asset to recover the outstanding debt. The major benefit here is that your personal home is generally not at risk, unlike a secured business loan where your house might be used as collateral. It's always best to contact your broker early if you anticipate cash flow issues to discuss your options.

Can I use asset finance for second-hand machinery from a private seller?

You can use asset finance for second-hand machinery purchased from a private seller, though the process involves a few extra steps. Lenders will usually require an independent valuation or inspection to ensure the asset is worth the purchase price. They also perform title checks to confirm the seller owns the equipment outright. While it's slightly more complex than buying from a dealership, it's a great way to save on capital costs while still securing professional funding.