You've finally found the ideal used truck to expand your fleet, but the big banks are stalling because the asset isn't fresh off the assembly line. It's incredibly frustrating to watch a great deal slip away while you're stuck in a loop of paperwork and confusion over "Low Doc" requirements. For many owner-drivers in 2026, securing used truck finance Melton feels like a race against time where the hurdles are constantly moving. We know you need a partner who understands that a well-maintained used vehicle is a strategic asset for your business, not a liability.

We agree that being self-employed shouldn't make getting a loan an uphill battle. This guide promises to show you exactly how to secure competitive finance tailored for sole traders, ensuring you don't miss out on the right vehicle. We will explore how to use tax-effective structures like a Chattel Mortgage to protect your cash flow, how to handle the updated 2026 mass limit regulations, and the fastest ways to get an approval that puts you back on the road with confidence.

Key Takeaways

- Identify why Melton’s booming logistics corridor makes used vehicle acquisition a strategic choice for protecting your business cash flow.

- Compare the benefits of Chattel Mortgages and Hire Purchase agreements to find the most tax-effective used truck finance Melton for your specific ABN setup.

- Learn how Low Doc finance options bypass the rigid requirements of big banks, allowing self-employed owner-operators to secure approvals with less paperwork.

- Follow a practical checklist to organise your ABN, GST registration, and financial statements for a streamlined application process.

- Discover the advantage of working with a local specialist who understands the unique demands of the transport and construction industries in Melbourne’s West.

Navigating Used Truck Finance in Melton’s Growing Logistics Hub

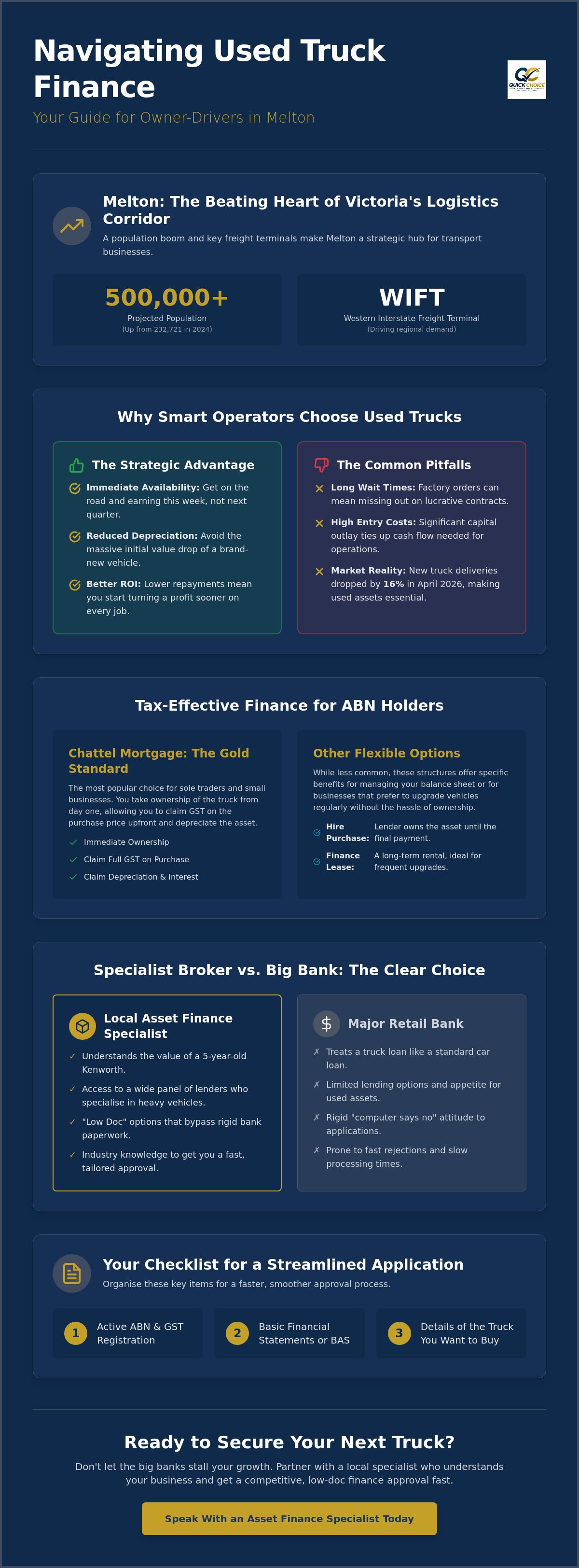

Melton has rapidly transformed from a quiet outer suburb into the beating heart of Victoria's Western Growth Corridor. With the local population projected to soar from 232,721 in 2024 to over 500,000 in the coming decades, the pressure on the transport network is immense. This explosion in growth, coupled with the development of the Western Interstate Freight Terminal (WIFT) in Truganina, has turned the region into a critical logistics node. For self-employed owner-drivers, being positioned in this hub offers a massive advantage, provided you have the right equipment to keep up with the pace.

Securing used truck finance Melton is often the most strategic move for contractors looking to scale. Unlike new vehicle lending, which involves long wait times and high entry costs, used finance allows you to acquire a reliable Commercial vehicle that’s ready for work immediately. In April 2026, new truck deliveries in Australia dropped by 16%, proving that the used market is now the primary engine for small business growth. Financing a used asset requires a different approach, as lenders focus on the vehicle's remaining service life and its ability to generate consistent cash flow for your business.

Why Melton Operators Prefer Used Assets

Local contractors are increasingly turning to the used market to avoid the significant capital outlay of new builds. Late-model trucks are entering the market in record numbers as large fleet operators cycle through their assets, giving sole traders access to high-spec machinery at a fraction of the cost. The benefits include:

- Immediate Availability: You can't afford to wait months for a factory order when a new contract starts next week.

- Reduced Depreciation: Let the first owner take the initial value hit while you enjoy a lower loan principal.

- Better ROI: Lower monthly repayments mean your truck starts turning a profit much sooner, which is vital for earthmoving and courier businesses.

The Role of a Specialist Asset Finance Broker

A city-based bank often treats a truck loan like a standard car loan, which is a mistake that leads to fast rejections. A local specialist understands that used truck finance Melton requires a deeper knowledge of the transport industry. We know that a five-year-old Kenworth or Hino is still a powerhouse asset with years of earning potential. Brokers provide access to a wider panel of lenders who specialise in heavy vehicles, ensuring you aren't limited by the rigid "Computer says no" attitude of the big four banks. Whether you’re buying from a dealer in Truganina or a private seller in Werribee, a specialist ensures the paperwork is handled correctly so you can secure the vehicle before it sells to someone else.

Financing Options for Self-Employed Owner-Operators in Melton

Selecting the right loan structure is just as critical as the horsepower under the bonnet. When you're searching for used truck finance Melton, you'll find that the landscape in 2026 favours flexibility for ABN holders. Most owner-operators aren't just looking for a way to pay for a vehicle; they're looking for a tax-effective tool that protects their monthly cash flow. Before committing to a rig, checking a comprehensive guide to buying a vehicle can help clarify the total cost of ownership beyond the initial sticker price.

While Chattel Mortgages dominate the market, Hire Purchase agreements and Finance Leases remain viable alternatives depending on your accounting setup. A Hire Purchase allows the lender to buy the truck and "hire" it to you until the final instalment is paid. This can be useful for managing the balance sheet, though it lacks some of the immediate tax perks of other structures. Finance Leasing, on the other hand, is often preferred by those who want to upgrade their truck every few years without the hassle of ownership. If you're unsure which path fits your specific tax strategy, you can speak with an asset finance specialist to compare these options side-by-side.

The Chattel Mortgage Advantage

For the 2025-2026 income year, small businesses with a turnover under $10 million can still benefit from the instant asset write-off for eligible assets costing less than $20,000. For larger used truck purchases, the Chattel Mortgage remains the gold standard. It allows you to claim the GST on the purchase price in your next BAS, providing an immediate boost to your working capital. Because you own the asset from day one, you can also claim depreciation and interest as tax-deductible expenses. This structure is particularly effective for Melton’s truckies who need to keep their overheads low while expanding their capacity.

Age and Condition: What Lenders Look For

Lenders are often cautious with older assets, typically enforcing a "10 to 15-year rule." This means the truck usually shouldn't be older than 15 years at the end of the loan term. If you’re eyeing a classic rig, your interest rate might be slightly higher to reflect the perceived risk. Lenders will scrutinise the vehicle's condition, especially in private sales where a dealer's guarantee is absent. To secure approval for an older model, you'll often need:

- A comprehensive pre-purchase inspection report from a qualified mechanic.

- Detailed maintenance records to prove the vehicle's longevity.

- A valuation to ensure the loan amount aligns with the truck's actual market value.

Navigating these age restrictions requires a proactive approach. Dealer sales are generally easier to finance because the paperwork is standardised, but private sales can offer better value if you have your documentation in order. We help you bridge that gap by ensuring the lender sees the value in the asset, regardless of where it's being sold.

Why Local Tradies Choose Specialist Brokers Over Big Banks

Walking into a major bank branch in Melton with a set of keys for a 2021 Isuzu often leads to a quick rejection. Big banks are built for PAYG employees with predictable pay slips; they frequently struggle to understand the fluctuating income of a self-employed truckie. This "Computer Says No" problem is a major roadblock for owner-drivers who need to move quickly on a vehicle. Securing used truck finance Melton shouldn't depend on whether a bank manager understands the logistics industry. While a bank offers you one set of rigid criteria, a specialist broker provides access to a panel of over 80 lenders, many of whom specifically target the heavy vehicle sector.

Specialist lenders are far more comfortable with non-standard income. Whether you're dealing with seasonal peaks in freight or you've recently started a new ABN, these lenders look at the strength of your contracts and your bank statements rather than just two years of perfect tax returns. They understand that a truck is a tool for generating revenue, and they evaluate the loan based on that earning potential. This flexibility is what allows local transport and construction businesses to stay competitive in a fast-moving market.

The Low Doc Revolution for Owner-Drivers

Low Doc Truck Finance has changed the game for owner-operators who don't have their latest tax returns finalised. If you've been trading with an active ABN and GST registration for at least 12 to 24 months, you can often qualify for finance using only your bank statements and a signed privacy form. This streamlined approach removes the administrative burden that usually stalls a loan application. The speed of approval is a significant advantage; brokers can often secure funding within 24 to 48 hours. This ensures you can pounce on a quality used truck before another buyer snaps it up.

Avoiding the Dealer Finance Trap

It's tempting to sign up for finance at the dealership while you're standing in front of the truck, but this often limits your options. Dealer finance is designed to move the stock on that specific lot, and the rates are rarely the best used truck finance Melton has to offer. You might face hidden fees or aggressive "balloon" payments that look good on paper but hurt your cash flow in the long run. By choosing an independent broker, you gain the freedom to buy from any seller across Victoria, including private sellers. For a deeper dive into these structures, our Asset Finance for Self Employed: The Ultimate 2026 Australian Guide provides a comprehensive roadmap for 2026.

Checklist: Preparing Your Used Truck Finance Application

Don't wait until you've found the perfect rig to start gathering your paperwork. While we've discussed how flexible the market has become, being prepared is what allows you to secure a vehicle before a competitor does. Lenders reviewing applications for used truck finance Melton want to see a clear picture of a stable, legitimate business. Start by verifying that your ABN is active and your GST registration is current. If you've recently changed your business structure or moved from a sole trader to a company setup, notify your broker early. These details change which lending products you qualify for.

Reviewing your credit score before the lender does is another vital step. Small oversights or old defaults can sometimes linger on your report, and it's better to address them upfront. Alongside your credit history, organise your internal profit and loss statements or your most recent Business Activity Statements (BAS). Even if you're pursuing a Low Doc path, having these documents ready acts as a safety net if a lender needs to verify a specific cash flow peak. You can speak to our team today to get a pre-approval so you can shop with confidence.

Essential Documentation for Melton Contractors

Most lenders require a standard set of documents to move your application through the system quickly. You'll need current Australian identification, typically a passport or a driver's licence. Speaking of licences, ensure yours is valid for the specific truck class you're financing, whether that's Heavy Rigid (HR), Heavy Combination (HC), or Multi-Combination (MC). For proof of income, have at least six months of bank statements ready to show consistent trading activity. This transparency helps lenders feel comfortable with the loan amount.

Evaluating the Truck Before You Buy

The truck itself is the security for the loan, so its condition and history matter immensely. You must check the Personal Property Securities Register (PPSR) to ensure the vehicle has no existing finance or a "written off" status. Always verify that the VIN and engine numbers on the truck match the registration papers exactly. Discrepancies here can stall a settlement for weeks. For a more detailed look at the current lending landscape for owner-operators, read our Self-Employed Truck Finance: The 2026 Guide. Ensuring the truck is mechanically sound and legally clear is the final piece of the puzzle for a successful application.

How Quick Choice Supports Melton’s Transport & Construction Businesses

Operating a transport business in Melbourne’s west requires more than just a reliable rig; it requires a financial partner who understands the local terrain. Our team specialises in used truck finance Melton, focusing specifically on the needs of self-employed owner-drivers in booming areas like Truganina, Werribee, and the Melton industrial precincts. We recognize that while you are busy managing deliveries or navigating construction sites, you don't have the time to sit in a bank manager's office explaining how your ABN works. We act as your advocate, translating your business success into a loan structure that lenders actually approve.

We believe in a supportive approach that treats you as a partner rather than just another application number on a screen. By streamlining the entire loan process, we handle the complex communications with lenders so you can stay focused on the road. Our commitment is to find tax-effective solutions that protect your cash flow, ensuring that your new used asset helps your business grow instead of becoming a financial burden. We look at the big picture, including how a specific loan might interact with your BAS cycles and EOFY requirements.

Bespoke Finance for Western Suburbs Operators

Our focus on self-employed professionals makes a tangible difference in the approval rates our clients experience. We understand the specific demands of the transport and construction sectors, providing direct support for a wide range of assets, including:

- Prime Movers: Securing competitive rates for heavy-duty long-haul vehicles.

- Rigid Trucks: Tailored options for local distribution and specialised trade vehicles.

- Trailers: Financing for refrigerated vans, flatbeds, or tippers to complete your setup.

We handle all the heavy lifting regarding documentation and lender negotiations. This bespoke service ensures that whether you are a solo operator or managing a small fleet, your finance is as adaptable as your business needs to be.

Start Your Journey Today

Taking the first step towards your next vehicle shouldn't be stressful. We provide transparent quotes that allow you to understand your potential repayments without negatively impacting your credit score. The Quick Choice promise is built on reliability and clear communication; we tell you exactly what is possible from the start. If you're ready to secure a vehicle and keep your business moving forward, we are here to guide you through every stage of the process.

Organise your used truck finance with Quick Choice today and experience a partnership designed for the modern Australian owner-driver.

Fuel Your Business Growth in Melbourne’s West

Securing the right equipment shouldn't be a source of stress for Melton’s hardworking owner-drivers. By choosing used assets and tax-effective loan structures, you're positioning your business to capitalise on the region's massive logistics expansion. We've explored how Low Doc options and specialist guidance can bypass the rigid barriers of big banks, giving you the speed and flexibility needed to thrive in 2026. As specialist brokers for self-employed Australians, we provide you with a direct path to over 80 trusted lenders who understand the true value of your fleet.

Success on the road starts with a financial plan that protects your cash flow while allowing for rapid scaling. Whether you are operating out of Truganina or managing deliveries across the Western Suburbs, our team is committed to providing the local support you deserve. Finding the most competitive used truck finance Melton is simply about having the right partner by your side. We take the guesswork out of the application process, ensuring your documentation is ready and your approval is fast. Get a quick quote on used truck finance in Melton today and let’s get your next vehicle on the road. Your business has a bright future, and we are ready to help you drive it there.

Frequently Asked Questions

Can I get used truck finance in Melton with a new ABN?

Yes, you can certainly secure finance even if your ABN has been active for less than 12 months. While many big banks require two years of trading history, specialist lenders offer "start-up" products for new owner-operators. You may need to demonstrate previous experience in the transport industry or provide a larger deposit to offset the lender's risk. We focus on your business's future potential rather than just its short history.

What is the maximum age for a truck to be financed?

Most lenders prefer the vehicle to be no more than 15 years old at the end of the loan term. For example, if you're looking at a five-year loan, the truck should ideally be 10 years old or newer at the time of purchase. Some specialised lenders will consider older rigs if they are in exceptional condition or are a highly sought-after model, though this may require a formal valuation or a mechanical report.

Is a deposit required for self-employed truck loans?

A deposit isn't always mandatory for established self-employed drivers with a clean credit history. Many of our lenders offer "no deposit" options for ABN holders who have been GST-registered for at least two years. However, putting down a deposit can be a smart move to reduce your monthly repayments and lower the total interest paid over the life of the loan, especially when securing used truck finance Melton for older assets.

What is a Chattel Mortgage and how does it help with tax?

A Chattel Mortgage is a commercial loan where you take ownership of the truck immediately while the lender uses the vehicle as security. This structure is highly popular because it typically allows you to claim the full GST on the purchase price in your next Business Activity Statement (BAS). Additionally, you can usually claim both the interest on the loan repayments and the vehicle's depreciation as tax deductions, which helps protect your business cash flow.

How long does the approval process take for used truck finance?

You can often receive a conditional approval within 24 to 48 hours of submitting your application. If you have your bank statements, identification, and ABN details ready, the process moves very quickly. Once the lender approves the loan and the vehicle inspection is complete, settlement can often occur within a few business days, allowing you to pick up your truck and get straight to work.

Can I buy a used truck from a private seller in Melton?

Yes, you have the freedom to purchase from a private seller rather than being restricted to a dealership. While private sales require a few extra steps, such as a PPSR check and a basic vehicle inspection, they often provide better value for owner-drivers. We handle the additional paperwork and coordinate with the seller to ensure the funds are transferred securely and the title is clear before you take delivery.

What happens if I have a low credit score but a strong ABN history?

A strong ABN history and consistent cash flow can often outweigh a less-than-perfect personal credit score. Specialist lenders understand that business owners sometimes face hurdles, and they prioritise your current ability to service the loan over past credit events. If your bank statements show a healthy, trading business, we can often find a lender who will work with you to secure the equipment you need.