Why does a solid day’s work and a healthy ABN turnover still lead to a "no" from the big banks just because your latest tax returns aren't finalised? If you are looking for sole trader ute finance Hoppers Crossing specialists, you likely already know that traditional lenders often fail to account for the way local contractors actually operate. It is frustrating to be held back by rigid paperwork requirements when you simply need a reliable new rig to stay on the job and keep your business moving forward.

We believe your finance should work as hard as you do. This guide reveals how to secure the best ute finance for your sole trader business, even with low-doc requirements that typically stall standard applications. You will learn how to leverage a chattel mortgage to claim GST credits quickly, understand the $20,000 instant asset write-off for the 2026 financial year, and find a streamlined path to getting your new Ford Ranger or HiLux on the road without the usual bank delays.

Key Takeaways

- Learn why local Hoppers Crossing specialists provide better outcomes than major banks for sub-contractors needing fast approvals.

- Understand the differences between Chattel Mortgages and Finance Leases to maximise your tax benefits and GST credits.

- Discover how to qualify for sole trader ute finance Hoppers Crossing using low-doc options that don't require years of finalised tax returns.

- Master the "51% rule" to ensure your new work vehicle qualifies for commercial interest rates and the 2026 instant asset write-off.

- Compare the best-performing 2026 utes, including the latest hybrid models, to balance on-site reliability with high resale value.

Why Sole Trader Ute Finance in Hoppers Crossing Requires a Local Specialist

Hoppers Crossing and the wider City of Wyndham have transformed into a powerhouse of independent trade activity. If you drive down Old Geelong Road or through the industrial precincts in Truganina and Laverton North, you will see exactly why local expertise matters. The Western Suburbs are no longer just a residential fringe; they are a critical hub for sub-contractors who keep Melbourne's infrastructure moving. Securing sole trader ute finance Hoppers Crossing isn't just about finding a loan. It is about partnering with someone who understands that your vehicle is a revenue-generating asset, not a personal luxury.

For a local tradie, a reliable dual-cab is more than transport; it is a mobile office, a tool shed, and a lifeline to every job site. When your finance is structured correctly, that ute pays for itself through increased efficiency and tax advantages. Working with a local specialist ensures you aren't treated like a number in a CBD high-rise. Instead, you get a partner who knows the local dealerships and understands the specific economic pressures facing Wyndham business owners in 2026.

Hoppers Crossing: A Hub for Independent Contractors

The rise of trade businesses near the Old Geelong Road commercial strip has created a unique micro-economy. Local sole traders are the backbone of this region, providing essential services to the thousands of new homes being built across Werribee and Tarneit. A finance specialist who lives and works in the West knows that your schedule is demanding. They prioritise speed and proximity to ensure you spend less time signing papers and more time on the tools. This local connection often means faster settlements because your broker can coordinate directly with nearby dealerships to finalise your sole trader ute finance Hoppers Crossing requirements.

The Downfall of Big Bank Ute Loans

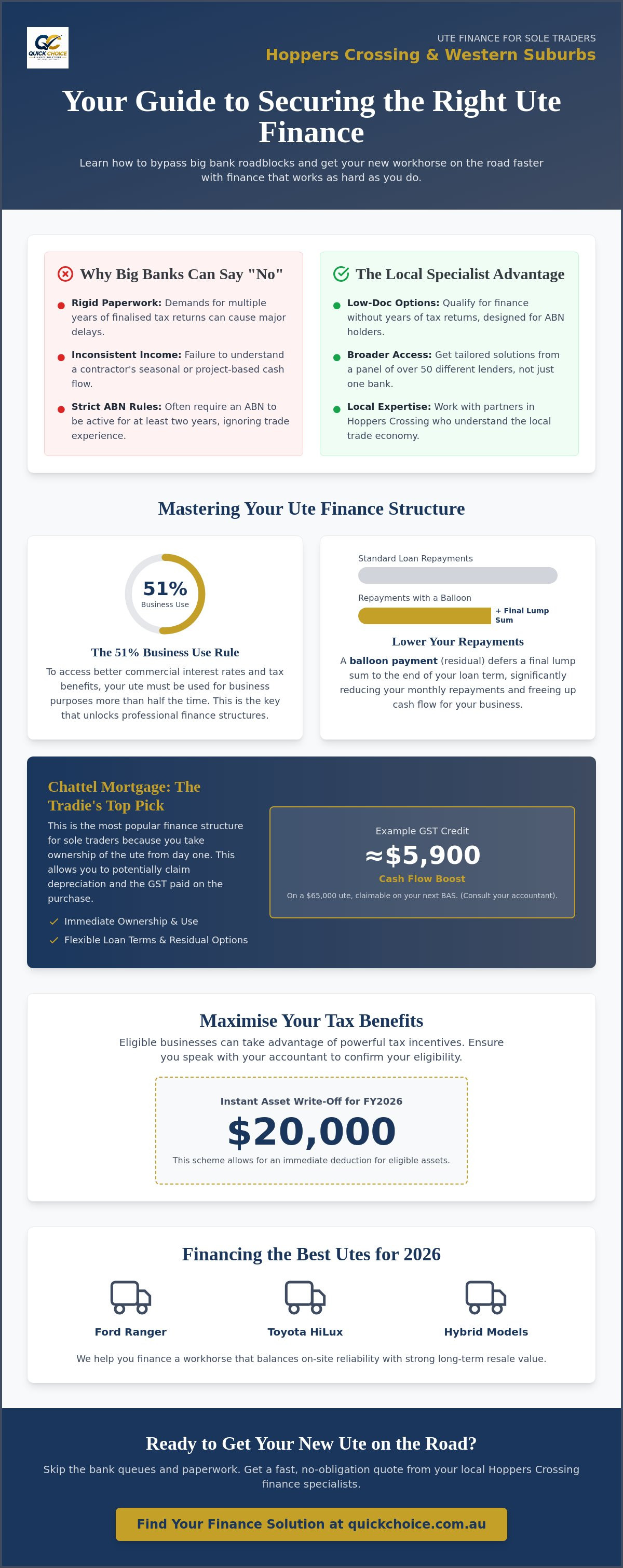

Standard consumer car loans often fail sub-contractors because they don't account for the realities of self-employment. Traditional banks frequently reject applications for the following reasons:

- Seasonal Income: Banks prefer steady, identical weekly pay slips, which rarely reflect a tradie's cash flow.

- ABN Age: Many lenders require an ABN to be active for two years, even if you have decades of experience in your trade.

- Paperwork Overload: The demand for full tax returns can stall an application for months.

A specialist broker looks beyond these rigid barriers. They focus on commercial structures like a Chattel Mortgage, which allows you to take ownership of the vehicle immediately. This structure is specifically designed for business use, offering potential GST input credits and depreciation benefits that a personal bank loan simply cannot provide. By choosing a broker with access to over 50 lenders, you gain options that a single bank branch in Werribee cannot match.

Understanding Ute Finance Structures for ABN Holders in 2026

Choosing the right setup for your sole trader ute finance Hoppers Crossing depends heavily on how you manage your tax and cash flow. Before you sign for that new Toyota HiLux or Ford Ranger, you must understand the 51% rule. To access commercial interest rates, which are typically more competitive than personal ones, you must intend to use the vehicle for business purposes at least 51% of the time. Meeting this requirement unlocks several professional finance structures designed to help your business grow while keeping your monthly overheads manageable.

One of the most effective ways to lower your monthly commitment is through a balloon payment, also known as a residual. This involves deferring a portion of the loan principal to the end of the term, which significantly reduces your regular repayments. For many sub-contractors in the Western Suburbs, this strategy keeps cash in the business for materials and equipment during the busy season. It is a practical way to drive a better vehicle without straining your weekly budget.

Chattel Mortgage: The Tradie's Favourite

The Chattel Mortgage remains the top choice for Hoppers Crossing sole traders who want ownership from day one. Because you own the asset immediately, you can generally claim the full GST component of the purchase price on your next Business Activity Statement (BAS). For a $65,000 ute, this can result in a GST input credit of approximately $5,900, providing a significant cash flow injection back into your business. You also have the flexibility to choose loan terms ranging from three to seven years, allowing you to align the finance with your specific project pipeline and expected vehicle turnover.

Finance Lease and Operating Leases

Leasing offers a different path for contractors who prefer to preserve their capital. Instead of owning the ute, the lender buys the vehicle and leases it back to you for a fixed monthly fee. This is often an attractive option for high-turnover businesses that want to upgrade their fleet every few years without the hassle of selling a used vehicle. While you don't build equity in the same way as a mortgage, the entire lease payment is usually tax-deductible if the vehicle is used solely for work. This structure can be particularly useful if you are looking to organise asset finance for the self-employed with minimal upfront costs.

Tax considerations for 2026 are also a major factor. For the 2025-2026 financial year, the instant asset write-off threshold remains at $20,000 for eligible assets. This applies to small businesses with an aggregated turnover of less than $10 million. If your ute purchase falls within these guidelines, you can deduct the cost immediately rather than depreciating it over several years. Even for vehicles above this threshold, you can still claim significant depreciation and interest deductions, making professional finance a powerful tool for reducing your overall tax bill.

How to Qualify for Low-Doc Ute Finance as a Sub-Contractor

Securing sole trader ute finance Hoppers Crossing does not always require a mountain of paperwork. In 2026, "low-doc" finance refers to a streamlined application process that avoids the need for full, accountant-prepared tax returns or profit and loss statements. This is particularly beneficial for sub-contractors whose income might be strong but whose latest tax filings are still being finalised. By focusing on current cash flow rather than historical data, lenders can offer approvals much faster than traditional banks.

Your credit history is the foundation of a successful low-doc application. Because the lender is asking for less financial documentation, they rely heavily on your repayment track record. A clean credit file signals that you are a reliable borrower, which often leads to fast-tracked approvals within 24 to 48 hours. If you have maintained a strong credit score, you can typically access finance for utes priced up to $100,000 without providing extensive proof of income.

The length of your ABN registration is the other critical factor. Most specialist lenders prefer to see an active ABN that has been registered for at least twelve months. For very established businesses with more than two years of ABN history and property ownership, a "no-doc" path may even be possible. This level of finance requires almost no financial evidence beyond a simple declaration of income and a clean credit check.

The 5-Step Low-Doc Approval Process

Getting your application ready doesn't have to be stressful. Follow these five steps to ensure you are prepared for a smooth approval:

- Step 1: Verify that your ABN and GST registration have been active for at least 12 months.

- Step 2: Prepare your business bank statements from the last three to six months to demonstrate consistent cash flow.

- Step 3: Confirm your property ownership status, as being a homeowner often unlocks lower interest rates and higher borrowing limits.

- Step 4: Request a pro-forma invoice from your dealership for the specific ute you intend to purchase.

- Step 5: Ensure your identification documents, such as your driver's licence and Medicare card, are current and ready for the 100-point check.

Common Pitfalls in Sole Trader Applications

Even with a strong turnover, simple mistakes can delay your sole trader ute finance Hoppers Crossing. One of the most frequent issues is mixing personal and business expenses in a single bank account. Lenders prefer to see a dedicated business account that clearly shows your trade-related income and outgoings. It makes it much easier for them to verify your business's health.

You should also be transparent about any existing equipment or tool loans. Failing to disclose these can lead to a rejection once the lender conducts their background checks. Finally, avoid making multiple credit enquiries in a short period. Every time you apply for finance, it leaves a mark on your credit file. Too many hits in a single month can make you appear desperate for credit, which may negatively impact your borrowing power.

Choosing the Right Workhorse: Financing the Best Utes in 2026

Selecting the right vehicle is about balancing daily performance with long-term financial health. In 2026, the Ford Ranger and Toyota HiLux continue to dominate the local landscape due to their high resale value and proven durability. When you look for sole trader ute finance Hoppers Crossing, consider how the vehicle’s 3.5-tonne towing capacity and payload limits align with your specific trade. A plumber has different needs than a landscaper, and your finance structure should reflect the longevity of the asset you choose.

Deciding between new and used involves more than just the sticker price. For a new ute, indicative interest rates for a chattel mortgage currently range from 5.79% to 9.49% p.a. If you opt for a used model, rates typically sit higher, between 6.99% and 12.49% p.a. While a used vehicle has a lower initial cost, the higher interest rate and potential maintenance issues can narrow the gap. Many local contractors find that the lower rates and full warranty of a new vehicle provide better peace of mind and more predictable cash flow.

Electric Utes (EVs) and Hybrid Options

The shift toward electrification is gaining momentum with the arrival of plug-in hybrid models like the BYD Shark. Choosing a hybrid or electric workhorse can significantly reduce your weekly running costs through lower fuel consumption. Many of these vehicles also benefit from specific tax treatments for commercial use, making them an efficient choice for the modern sub-contractor. Some specialist lenders now offer "Green" asset finance discounts, providing lower interest rates for low-emission vehicles to encourage the transition to a sustainable fleet.

Financing Accessories and Fit-outs

Your ute isn't ready for work until it is fitted with the right gear. Whether you need heavy-duty canopies, toolboxes, or ladder racks, you can often include these fit-outs in your total loan amount. It is usually more cost-effective to finance these additions at the point of purchase rather than paying cash later. This approach ensures your entire work setup is covered under one manageable monthly payment. You should also ensure your insurance policy covers both the vehicle and the specialised business equipment installed to avoid out-of-pocket expenses if an accident occurs.

If you are ready to compare your options and secure a competitive rate, you can organise asset finance for the self-employed today and get an expert's view on your borrowing capacity for your next workhorse.

Why Quick Choice is the Preferred Ute Finance Partner in Hoppers Crossing

Quick Choice understands that for a Hoppers Crossing contractor, time away from the tools is money lost. We have built our reputation on deep expertise within the Hoppers Crossing and Werribee business community, ensuring that local sub-contractors get the support they deserve. When you search for sole trader ute finance Hoppers Crossing, you need more than a generic loan; you need a finance structure that treats your ABN as a valuable asset. We live and work in the same Western Suburbs streets as our clients, which gives us a unique perspective on the local economic growth and the challenges you face.

Our access to a panel of over 50 lenders, including specialist commercial funders, means we can find options that big banks often overlook. We don't just look at a single set of criteria. Instead, we match your specific business situation, whether you are a newly registered ABN or an established local veteran, with the lender most likely to offer a fast approval and a competitive rate. This tailored approach is designed to maximise your 2026 tax position, ensuring you benefit from every available deduction and GST credit discussed earlier in this guide.

The Quick Choice Advantage for Local Contractors

We speak your language. There is no confusing jargon or corporate gatekeeping here; we provide straightforward finance solutions that make sense for your business. Our streamlined application process happens primarily over the phone, meaning you can get the ball rolling while you are between jobs or on your lunch break. We prioritise speed because we know that a missing vehicle is a missing income. Our team works behind the scenes to handle the heavy lifting, from lender negotiations to coordinating with local dealerships in the Wyndham area.

We pride ourselves on fast approvals that get you back on the road and on the job site with minimal disruption. Our relationship with clients doesn't end when the papers are signed. We aim to be a supportive partner for the life of your business, helping you scale and upgrade your equipment as your workload grows. Whether you are looking for your first workhorse or managing a small fleet, we provide the consistent, reliable guidance you need to stay ahead of the competition.

Ready to Upgrade Your Workhorse?

If you are looking to expand your fleet or replace an ageing rig, now is the time to act. You can read more about how we help independent professionals in our guide on Asset Finance for Self Employed. For those specifically looking at vehicles, we recommend exploring our Business Vehicle Finance Australia options to see which structure fits your 2026 goals. Our Hoppers Crossing team is ready to help you navigate the complexities of ABN finance. Contact us today for a tailored quote that reflects your hard work and business potential.

Secure Your Next Workhorse with Confidence

Securing the right commercial vehicle is one of the most significant investments you will make as an independent professional. By choosing a structure like a chattel mortgage, you can maximise your 2026 tax benefits while keeping your cash flow steady for daily operations. Whether you are eyeing a new hybrid model or a classic diesel workhorse, the path to approval is much smoother when you have a partner who understands the local Wyndham market.

At Quick Choice, we specialise in low-doc and no-doc finance for those who don't have the time for endless bank paperwork. We provide access to over 50 Australian lenders, ensuring you get a tailored solution that fits your specific trade. If you are ready to take the next step with sole trader ute finance Hoppers Crossing, our team is here to handle the complexity so you can stay focused on the job at hand.

Get a tailored ute finance quote for your ABN today and experience the difference that local expertise makes for your business growth. We look forward to helping you get on the road.

Frequently Asked Questions

Can I get ute finance if I've only had my ABN for 6 months?

Yes, it is possible to secure finance with a six-month ABN, though your options are more limited than if you had a year of trading history. Most major lenders prefer at least 12 months of active ABN and GST registration. However, specialist commercial funders can often provide a solution if you have a clean credit history and a reasonable deposit to reduce the lender's risk.

What is the difference between a tradie ute loan and a personal car loan?

A tradie ute loan is a commercial finance product, such as a chattel mortgage, designed specifically for business use. Unlike a personal car loan, a commercial structure allows you to claim the GST on the purchase price and deduct interest and depreciation against your business income. These products often feature lower interest rates because the vehicle is viewed as a revenue-generating asset rather than a personal expense.

Do I need to be registered for GST to get sole trader ute finance?

You don't strictly need to be registered for GST to qualify for sole trader ute finance Hoppers Crossing, but it is often beneficial. Lenders generally offer more competitive rates and higher borrowing limits to GST-registered businesses because it signals a higher level of professional operation. If you aren't registered, you can still access finance, but you won't be able to claim the GST input credit on your purchase.

What is a balloon payment, and should I include one in my ute loan?

A balloon payment is a lump sum you agree to pay at the end of your loan term, which significantly reduces your regular monthly repayments. Including one can be an excellent strategy for sole traders who want to keep their weekly overheads low to manage cash flow. At the end of the term, you can choose to pay the balance, refinance it, or trade the ute in for a newer model.

Can I claim the full cost of my ute as a tax deduction in 2026?

In the 2025-2026 financial year, the instant asset write-off threshold is $20,000 for eligible small businesses with an aggregated turnover of less than $10 million. If your ute costs more than $20,000, you cannot claim the full cost immediately. Instead, you will claim a deduction for the vehicle's depreciation over several years, along with the interest paid on your loan and the general running costs of the vehicle.

How long does it take to get a ute loan approved in Hoppers Crossing?

Approval for sole trader ute finance Hoppers Crossing typically takes between 24 and 48 hours when you work with a specialist broker. Because we understand the specific documentation required for sub-contractors and have direct links to local dealerships, we can fast-track the process. Once your application is approved, settlement and vehicle pickup usually occur within a few business days, provided the vehicle is in stock.

Is it better to buy a new ute or a used one for my sole trader business?

Buying new often provides better financial value because interest rates for new utes currently range from 5.79% to 9.49% p.a., while used rates are higher, between 6.99% and 12.49% p.a. A new vehicle also comes with a full manufacturer's warranty and lower maintenance costs. While the initial purchase price is higher, the lower interest and increased reliability often make a new ute the more cost-effective choice for a busy contractor.

What happens if I use my ute for personal trips on the weekend?

You can use your work vehicle for personal trips, but you must ensure it is used for business purposes at least 51% of the time to qualify for commercial finance rates. For tax purposes, it's essential to keep an accurate logbook to track your business versus private kilometres. This allows your accountant to correctly calculate your deductions for fuel, insurance, and interest based on the actual business usage of the vehicle.