Why does a major bank treat a successful contractor like a financial risk just because their paperwork doesn't fit a standard template? If you've ever been knocked back for tradie van finance due to your low doc status or a missing tax return, you know that the traditional lending system often feels rigged against small operators. It's frustrating to face rigid requirements and confusing jargon when you simply need a reliable vehicle to get to the next job site and grow your business.

We agree that your business deserves better than a one-size-fits-all approach that drains your cash flow with unnecessarily high interest rates. This 2026 guide provides the expert path to securing a loan that actually works for you, focusing on speed, precision, and tax efficiency. You'll discover how to navigate the current $20,000 instant asset write-off rules, understand the $69,674 depreciation limit, and choose a loan structure that protects your bottom line. We will break down everything from the latest interest rate trends to the specific alternative documents you can use to bypass the mountain of bank paperwork and get your new workhorse on the road.

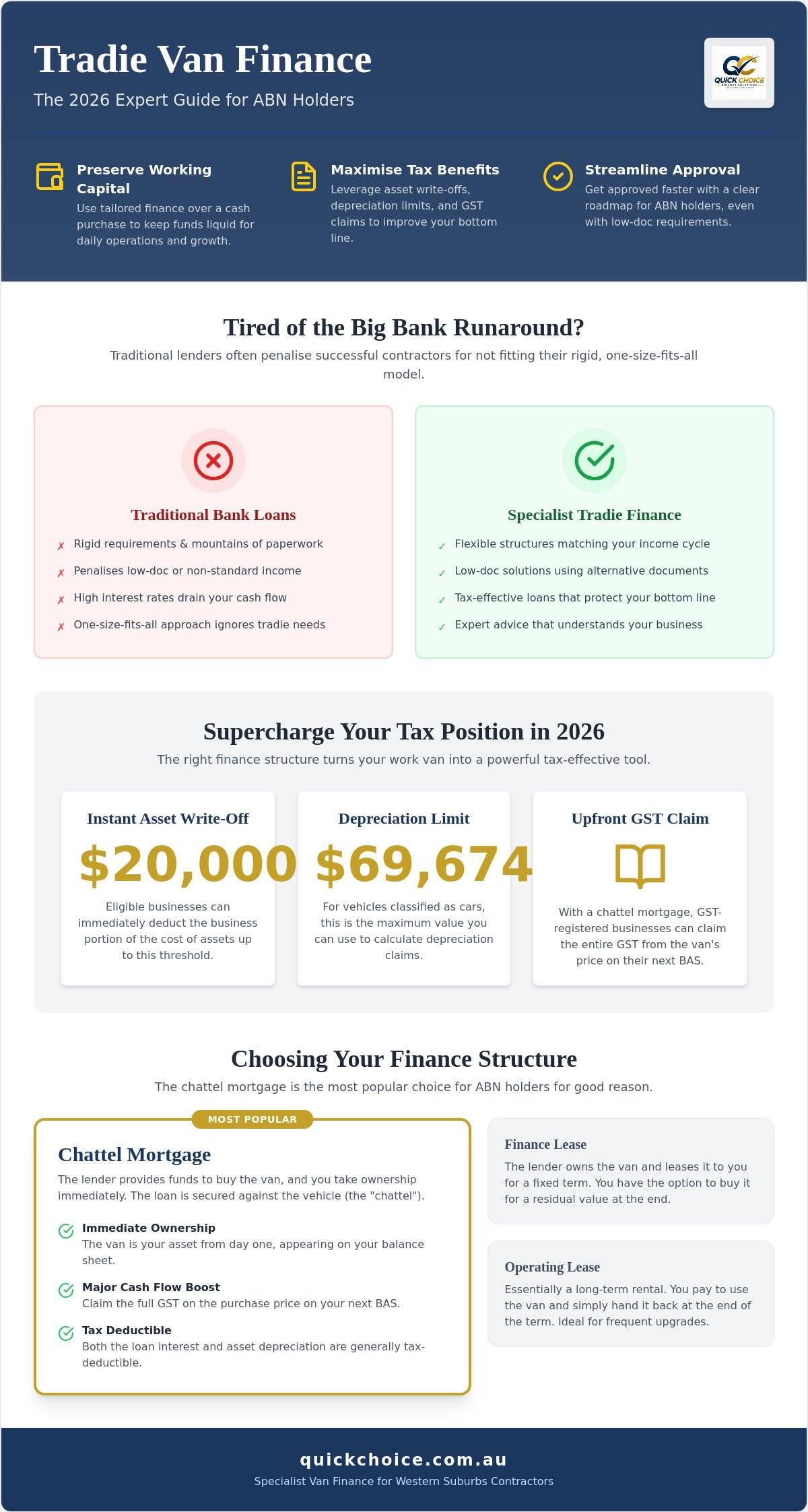

Key Takeaways

- Preserve your working capital by choosing tailored finance over a cash purchase, ensuring you have the liquid funds needed to manage daily operations and growth.

- Navigate the benefits of a chattel mortgage, the most popular structure for tradie van finance in 2026 due to its upfront GST claims and flexible repayment options.

- Maximise your tax position by understanding how to leverage the $20,000 instant asset write-off and the $69,674 depreciation limit for business vehicles.

- Streamline your approval process with a clear roadmap designed for ABN holders, even if you don't have the full financial documentation typically required by big banks.

- Gain a competitive edge in Melbourne's Western Suburbs by partnering with a specialist who understands the unique needs of local contractors and sole traders.

Why Securing the Right Business Van Loan is a Game-Changer for Sole Traders

Your work van is far more than just a way to get from point A to point B. For a sole trader or contractor, it's the engine room of your daily operations. When you secure the right tradie van finance, you aren't just taking on debt; you're making a strategic investment in your ability to scale. A reliable, modern vehicle allows you to take on larger courier runs or more complex service contracts without the constant fear of a breakdown. Beyond the mechanical reliability, a clean, sign-written van serves as a mobile billboard. As you drive through the streets of Melbourne, your brand gains visibility, turning every traffic jam into a marketing opportunity.

Many small operators feel tempted to buy a used van outright with cash to avoid interest. While this seems frugal, it often traps your working capital in a depreciating asset. Financing allows you to keep that cash for stock, materials, or emergency repairs. Making the psychological shift from "debt is bad" to "smart investment" is what separates growing businesses from those that stay stagnant. By choosing a Chattel Mortgage Explained structure, you can often claim the GST and interest as business expenses, making the loan a powerful tax-effective tool.

Cash Flow Management for Contractors

Managing cash flow is the biggest hurdle for any independent professional. Standard bank loans often demand rigid monthly payments that don't account for your busy and quiet periods. Specialist asset finance for self employed is designed to be more flexible, allowing you to match your repayments to your actual income cycles. Avoid the trap of using personal credit cards for vehicle costs. High interest rates on cards can quickly spiral, whereas dedicated tradie van finance offers much lower rates and clearer structures. Keeping your business and personal finances separate ensures you maintain a healthy emergency buffer for when things get quiet.

Professionalism and Reliability

Time is literally money when you're on the tools. An old, unreliable van doesn't just cost you in mechanics' bills; it costs you in lost reputation. If you can't make it to a job in Tarneit or Werribee because your engine won't start, you risk losing that client forever. A modern workhorse ensures you meet your service level agreements every time. It also sends a clear message of professionalism. When you pull up to a client's driveway in a well-maintained vehicle, you command a higher level of trust and respect, which often allows you to justify premium pricing for your services.

Navigating Van Finance Options: Chattel Mortgages, Leases, and Low Doc Loans

Choosing the right way to fund your vehicle is just as vital as picking the van itself. Big banks often push generic personal loans that don't account for the unique tax needs of a business. For most ABN holders in 2026, the search for tradie van finance begins and ends with the chattel mortgage. This structure remains the most popular choice because it treats the vehicle as a business asset from day one. Unlike a personal loan, a chattel mortgage allows you to take ownership immediately while the lender secures the loan against the van.

If you prefer not to have the asset on your balance sheet, a finance lease or operating lease might suit your needs. In a finance lease, the lender buys the van and leases it to you; you then have the option to purchase it at the end of the term for a residual value. An operating lease is more like a long-term rental where you hand the keys back at the end, which is excellent for those who want to upgrade to the latest model every few years. For specific accounting setups, a Commercial Hire Purchase (CHP) offers a middle ground where you gain ownership only after the final payment is made.

The Power of the Chattel Mortgage

The standout benefit of a chattel mortgage is the impact on your cash flow. If you're GST-registered, you can typically claim the entire GST component of the van's purchase price on your next Business Activity Statement (BAS). This often results in a significant refund early in the loan term. You also benefit from depreciating the asset and claiming interest charges as tax deductions. To keep monthly repayments low, many contractors opt for a balloon payment at the end of the term. This helps keep your overheads lean while you're busy growing your client base in Melbourne's West.

Low Doc and No Doc Solutions

The "Low Doc" revolution has changed the game for sole traders who haven't yet finalised their latest tax returns. Lenders now look at alternative proof of income, such as six months of clean bank statements or Business Activity Statements. A clean credit history is your best friend here; it proves you're a reliable borrower even without a mountain of paperwork. If you're a new business or a contractor with a complex income stream, equipment finance for sole traders provides a streamlined path to approval that big banks simply can't match. If you're unsure which path fits your current turnover, it's worth seeing how a specialist brokerage can simplify these options for you.

Choosing Your Workhorse: Evaluating Costs, Tax Benefits, and ROI

Selecting the right vehicle is a balancing act between upfront cost and long-term efficiency. While a used van offers a lower entry point, it often carries higher maintenance risks that can derail your schedule. A brand-new vehicle provides the security of a manufacturer's warranty, ensuring your business stays mobile. For those looking at tradie van finance, it's essential to weigh fuel efficiency and payload capacity against your specific niche. A courier might prioritise a high-roof layout for volume, while a plumber needs heavy-duty racking and a high payload. In areas like Hoppers Crossing, electric vans (EVs) are becoming a viable option for local runs, offering significantly lower running costs despite a higher initial price tag.

Every dollar you spend on your vehicle should work as hard as you do. Calculating the cost per kilometre is a great way to see the true impact on your bottom line. If you're frequently stuck in West Melbourne traffic, a more fuel-efficient or hybrid model could save you thousands over the life of the loan. Don't just look at the monthly repayment; look at the total cost of ownership, including insurance, servicing, and registration.

The Tax Equation for ABN Holders

For the 2025-2026 income year, the instant asset write-off threshold is $20,000 per asset for businesses with an aggregated turnover of less than $10 million. This allows you to claim an immediate deduction for the full cost of eligible assets. If your van exceeds this amount, you'll typically use general depreciation rules. The car limit for the 2025-26 income year is $69,674, which caps the maximum cost you can use for depreciation on passenger vehicles. Remember to track your personal versus business use carefully. Using a logbook ensures you only claim the business portion of your tradie van finance interest and running costs, keeping you on the right side of the ATO. We always recommend consulting with your accountant to ensure your finance structure aligns perfectly with your broader tax strategy.

Calculating Your Return on Investment

A new van should be a tool that increases your earning potential. If a larger payload allows you to carry more materials and complete three jobs a day instead of two, the finance payment practically covers itself. Reliability is a major factor here. Every day your van spends in the workshop is a day you aren't earning. ROI in the context of van finance is the measure of how much additional revenue and time-saving a vehicle generates compared to the total cost of its repayments and maintenance. Factoring in the peace of mind that comes with a new vehicle allows you to focus on your craft rather than your transport.

The Application Roadmap: Getting Approved for Van Finance in Melbournes West

Getting your van on the road shouldn't feel like a second job. While some major lenders promise an instant digital decision, these automated systems often struggle to interpret the nuances of a contractor's income. A successful application for tradie van finance requires a methodical approach that respects your time and protects your credit file. Following a clear roadmap ensures you secure a competitive rate while maintaining the flexibility your business needs.

- Step 1: Organise your essentials. You'll need an active ABN, your driver's licence, and basic bank statements. Lenders typically look for consistent cash flow over the last six months rather than just a single, outdated tax return.

- Step 2: Define your budget. Determine your monthly repayment limit and decide on a balloon payment percentage. A balloon payment can significantly lower your ongoing costs, keeping your business lean during quieter months.

- Step 3: Secure pre-approval. Walking into a dealership with finance already sorted changes the dynamic. It turns you into a cash buyer in the eyes of the salesperson, giving you much more leverage to negotiate a better price on the vehicle.

- Step 4: Finalise and sign. Once you've picked your workhorse, the final invoice is matched to your approval. You sign the documents, and the funds are usually settled within 24 to 48 hours.

Local Considerations for Western Suburbs Tradies

Proximity matters when you're managing a busy schedule. Tradies working near Melton, Rockbank, or Caroline Springs have access to some of the state's largest commercial vehicle hubs. When selecting your van, ensure it meets the specific requirements of local infrastructure projects, such as the West Gate Tunnel or regional road upgrades. Working with a self employed finance specialist who understands these local dynamics is far more effective than calling a generic bank call centre. They can help you structure your tradie van finance to suit the specific demands of the Melbourne market.

Common Pitfalls to Avoid

Protecting your credit score is vital. Many contractors make the mistake of applying with multiple lenders simultaneously, which can leave "hard marks" on your credit file and lower your score. You should also look beyond the sticker price. Always factor in on-road costs like registration, insurance, and any custom shelving or racking you'll need. Over-leveraging is another risk; ensure your repayments don't choke your business growth or leave you without a cash buffer. If you're ready to see what's possible for your business, you can apply for van finance today and get a clear picture of your borrowing power.

Partnering with Quick Choice: Specialist Van Finance for Western Suburbs Contractors

Success in business is rarely a solo journey. When you're looking for tradie van finance, you need a partner who understands that your ABN is more than just a number on a tax form. We act as your Reliable Specialist Guide, transforming a complex application into a streamlined path forward. Unlike the rigid algorithms used by major banks, we take the time to look at the person behind the business. We know that a "no" from a computer doesn't reflect the true potential of a hard-working contractor.

Our team has a deep connection to the local business landscape. Whether you're based in Truganina or Tarneit, we understand the specific infrastructure demands and growth opportunities in Melbourne's West. We don't just want to help you secure your first workhorse; we're here to support your long-term ambition. As your business scales, we'll be by your side to help you grow from a single van to a full fleet of five or more vehicles. This long-term partnership ensures your finance structure remains as agile as your business.

Why Experience Matters in Asset Finance

Navigating the documentation requirements for independent contractors can be a minefield. We specialise in addressing the specific documentation gaps that often stall applications at generic institutions. By accessing a wide panel of specialised lenders, we find the tradie van finance product that fits your current turnover and future goals. This bespoke approach significantly reduces the stress of the process. It allows you to stay focused on your trade while we handle the heavy lifting of the finance application, ensuring you get the right result without the usual bank headaches.

Get Started Today

Taking the first step is simple and direct. When you reach out to our team, you'll speak with a local expert who understands the Western Suburbs market. During your initial consultation, we'll discuss your budget, your equipment needs, and the best tax-effective structure for your situation. We'll provide a clear list of what's required, so there are no surprises or hidden delays. Our goal is to get you behind the wheel as quickly as possible. You can secure your business van finance with Quick Choice today and get the reliable support your business deserves.

Drive Your Business Forward with the Right Workhorse

Securing the right tradie van finance isn't just about getting a set of keys; it's about building a foundation for sustainable growth. By choosing a tax-effective chattel mortgage and leveraging the 2026 instant asset write-off, you keep your cash flow healthy while adding a powerful asset to your balance sheet. You've seen how a modern, reliable van reduces downtime and projects the professional image your clients expect in Melbourne's West. It's time to stop letting rigid bank criteria hold your ambition back.

At Quick Choice, we specialise in removing the obstacles that often stand between self-employed contractors and the equipment they need. As specialist brokerage experts with deep local knowledge of the Western Suburbs, we provide direct access to a wide lender panel that understands ABN-specific requirements. We don't rely on generic bank algorithms; we focus on your unique business potential. Ready to upgrade your mobile office? Start your business van loan application with Quick Choice today. Your next job is waiting, and we're here to help you get there with confidence.

Frequently Asked Questions

Can I get a business van loan with a new ABN?

Yes, you can secure tradie van finance with a new ABN, though your options depend on how long you've been trading. While many traditional banks prefer at least two years of history, specialist lenders offer solutions for businesses trading for as little as six months. You'll generally need a clean credit history and may be required to provide a deposit to offset the lender's risk during the early stages of your operation.

What is a balloon payment and should I include one in my van loan?

A balloon payment is a lump sum you pay at the end of your loan term to reduce your monthly repayments. It's a popular choice for contractors who want to keep their ongoing overheads low and preserve cash flow for daily materials and stock. At the end of the term, you can choose to pay the amount in full, refinance the remaining balance, or sell the van to cover the cost.

Do I need to be GST registered to get a business van loan?

You don't need to be GST registered to apply for a business van loan, but being registered can provide significant tax advantages. For example, GST-registered businesses can typically claim the GST on the van's purchase price as an upfront credit in their next Business Activity Statement. If you aren't registered, you can still access finance, but you won't be able to claim those specific GST credits.

How much deposit do I need for a commercial van loan in Australia?

Many established sole traders can secure a commercial van loan with a A$0 deposit, depending on their credit profile and time in business. For new ABN holders or those using low-doc options, providing a deposit of 10% to 20% can often help you secure a more competitive interest rate. This upfront contribution reduces the lender's exposure and demonstrates your financial commitment to the asset.

Is the interest on my van loan tax-deductible for my sole trader business?

Yes, the interest component of your loan and the vehicle's depreciation are generally tax-deductible, provided the van is used for business purposes. You must track your business use versus personal use via a logbook to ensure you only claim the correct percentage. This makes tradie van finance a highly tax-effective way to acquire a new workhorse while lowering your overall taxable income.

What is the difference between a car loan and a business van loan?

A business van loan is designed specifically for ABN holders and offers different tax treatments compared to a standard consumer car loan. Business loans often allow for GST claims and higher depreciation limits, which are capped at A$69,674 for the 2025-26 income year. Consumer loans are generally paid with after-tax dollars and don't offer the same level of commercial flexibility or tax benefits.

Can I finance a used van from a private seller or only from a dealer?

You can finance a van from both private sellers and licensed dealerships, though the process for private sales involves a few extra verification steps. Lenders will typically require a professional valuation or inspection to ensure the vehicle's value matches the loan amount. They also perform a PPSR check to ensure the van is free of existing debt before transferring funds directly to the seller's account.

How long does the approval process take for a low-doc van loan?

The approval process for a low-doc van loan is remarkably fast, often taking between 24 and 48 hours. Because these loans rely on alternative documents like bank statements rather than full tax returns, the assessment is streamlined. Once you provide your identification and income proof, a specialist broker can often secure a formal approval within a single business day.