Imagine you're halfway through a busy spring season when your primary zero-turn mower finally packs it in. Without a spare $20,000 ready to go, the fear of losing contracts to the competition becomes very real. You need a landscaping equipment loan that works as hard as you do, but traditional banks often make you jump through hoops just because you're self-employed.

It's frustrating when your business is growing yet your paperwork hasn't quite caught up with your ambition. We understand that as an Aussie sole trader, you need finance that respects your seasonal income and offers flexible Low Doc options. This guide simplifies the process, showing you how to master equipment finance to scale your operations and win bigger jobs with the latest machinery.

We'll break down the 2026 instant asset write-off rules, compare the tax benefits of different loan structures, and show you how to get approved quickly so you can stay on the tools and keep your business moving forward. Whether you're eyeing a new excavator or a fleet of commercial mowers, we've got the insights to help you grow.

Key Takeaways

- Upgrade your fleet to reduce manual labour and take on larger, more profitable contracts with high-end machinery.

- Secure a landscaping equipment loan even without full financial records by leveraging Low Doc options designed for Aussie sole traders.

- Understand the differences between a chattel mortgage and leasing to choose the ownership structure that suits your specific tax requirements.

- Expand your business capabilities beyond basic tools by financing heavy-duty assets like mini-loaders, excavators, and site-prep gear.

- Streamline your application through a specialist broker who understands the Melbourne landscaping industry and handles the legwork with over 40 lenders.

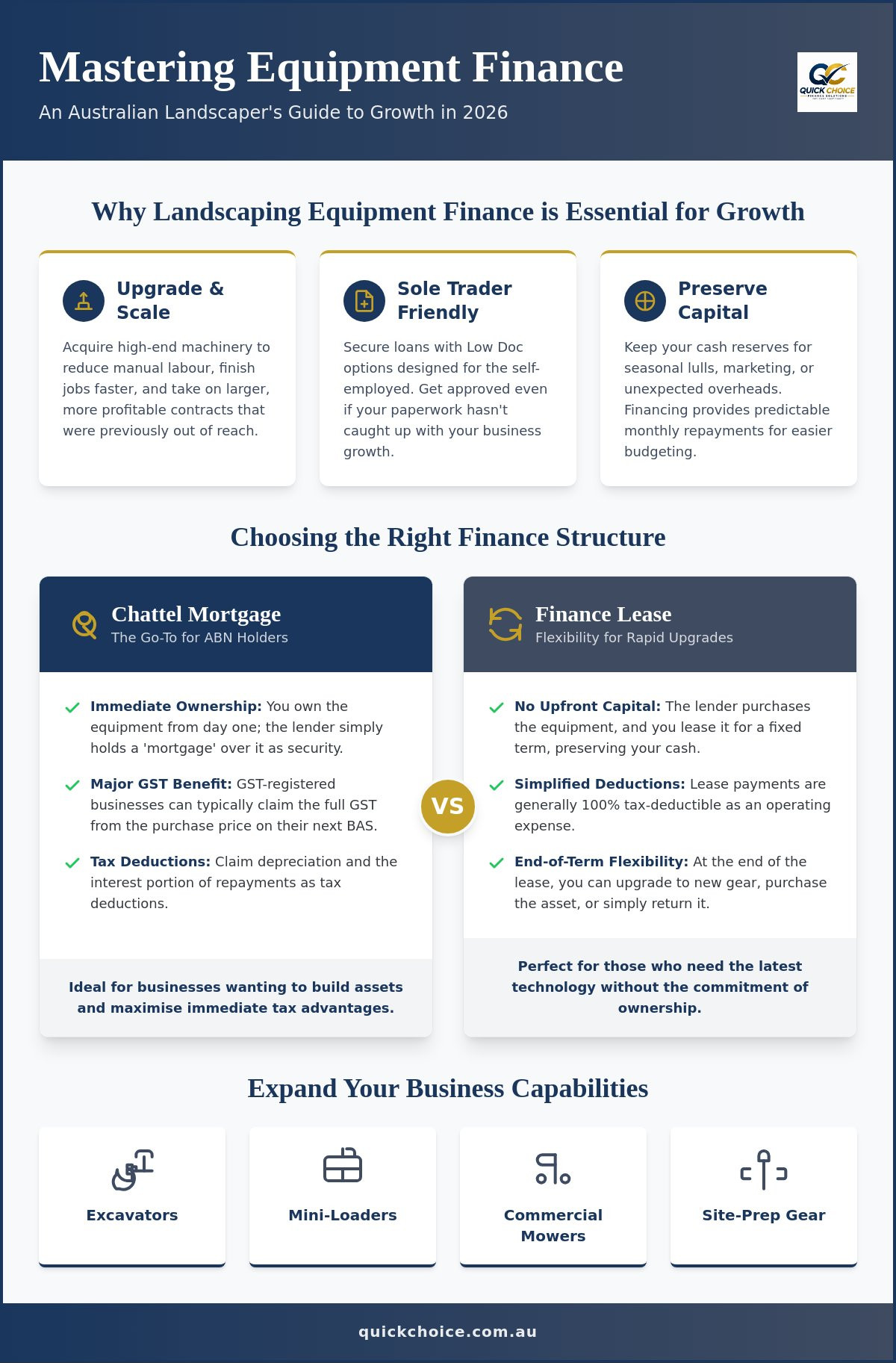

Why Landscaping Equipment Finance is Essential for Growth in 2026

Success in the landscaping industry isn't just about how well you can lay turf or build a retaining wall. It's about having the right tools for the job. A landscaping equipment loan is a strategic business tool that allows you to acquire high-value machinery without draining your bank account. Instead of waiting years to save for a new skid steer, you can get it on site now and let the equipment generate income immediately. This approach turns a potential liability into a productive asset from day one.

In 2026, the demand for professional landscaping across Melbourne’s new housing estates is surging. Developers and homeowners are looking for fast, polished results. Modern gear reduces your labour costs and significantly increases project turnaround speed. When you can finish a job in three days instead of five, you're not just saving time; you're increasing your capacity to take on more work. This efficiency is the difference between a business that survives and one that scales. With the Australian landscaping market projected to grow at over 6% annually from 2026, the competition is heating up.

Think of it as Equipment ROI. If a new machine costs $1,200 a month in repayments but allows you to bill an extra $4,000 in monthly revenue, the asset is effectively paying for itself. This shift in mindset transforms a landscaping equipment loan from a debt into a growth engine. It allows you to bid on larger contracts that were previously out of reach due to equipment limitations.

The Opportunity Cost of Outdated Machinery

Outdated machinery is a silent profit killer. Every hour your bobcat spends in the shop for repairs is an hour you aren't earning. Beyond the direct repair bills, there's the cost of project delays and the potential damage to your reputation. Newer gear allows for more competitive quoting on big jobs because you can guarantee timelines. It also meets the latest 2026 safety and compliance standards. Many site managers on larger projects won't even let you through the gates with aged equipment that lacks modern safety features.

Financing vs. Paying Cash: Preserving Your Working Capital

For many sole traders, cash is king. Landscaping is a seasonal trade, and having a healthy cash reserve is vital for navigating the quieter months. While paying cash might seem cheaper upfront, it strips your business of liquidity. Financing through a chattel mortgage or a finance lease keeps your emergency fund intact for unexpected overheads or marketing. It provides predictable monthly repayments that make budgeting much easier for independent contractors. You don't have to worry about a massive capital outlay that leaves you vulnerable if a client is late on a payment.

Choosing the Right Finance Structure: Chattel Mortgage vs. Leasing

Selecting the right landscaping equipment loan isn't just about the interest rate. It's about how the debt sits on your balance sheet and who technically owns the machine while you're out digging trenches. A specialist broker acts as your guide here, filtering through dozens of lenders to find a structure that aligns with your specific tax strategy. They help you weigh up immediate ownership against long-term flexibility.

One popular feature for sole traders is the "balloon payment" option. This allows you to defer a percentage of the loan amount until the end of the term. By doing this, you significantly lower your monthly commitments. This keeps your cash flow steady during the slower winter months when the ground is often too hard or too wet for major projects. It's a practical way to manage your overheads without sacrificing the quality of your gear.

The Chattel Mortgage: The Go-To for ABN Holders

For many tradies across Werribee and Tarneit, the chattel mortgage is the preferred path. You take ownership of the gear from the moment you leave the dealership. The lender simply takes a "mortgage" over the asset as security. The biggest drawcard here is the GST benefit. If you're GST-registered, you can generally claim the full GST amount on the purchase price in your very next Business Activity Statement (BAS). This provides a significant cash injection back into your business early on.

Finance Leasing: Flexibility for Rapid Upgrades

Leasing works differently. The lender buys the equipment and "leases" it back to you for a set period. This is ideal for landscapers who want the latest tech every few years without the hassle of selling old gear. Your lease payments are usually fully tax-deductible as a business expense. At the end of the term, you have three main choices:

- Return the equipment to the lender and walk away.

- Upgrade to a newer, more efficient model with a fresh lease.

- Make an offer to purchase the asset outright for its residual value.

While you're looking at finance options, it's also worth checking government grants and programs to see if there's additional support available for your business expansion. If you're unsure which path fits your ABN best, you can speak with an expert broker to compare your options and find the right fit for your specific circumstances.

Qualifying for a Loan as a Self-Employed Landscaper

Many landscapers put off upgrading their machinery because they dread the perceived interrogation from big banks. The common fear is that without two years of perfect tax returns, a landscaping equipment loan is out of reach. In reality, the lending market in 2026 is far more nuanced. Specialist lenders now prioritise your current cash flow and industry experience over stacks of historical paperwork.

The "Low Doc" or Low Documentation path is specifically designed for sole traders in this position. If you have an active ABN and have been registered for GST for at least 12 months, you've already cleared one of the biggest hurdles. Lenders look at your business story; they want to see that you understand your market and have a clear plan for how the new equipment will increase your earnings. Providing evidence of upcoming projects or signed maintenance contracts can often carry more weight than a tax return from two years ago.

The New ABN Challenge

If you've been trading for less than 12 months, you might feel like you're in a "no-man's land" for finance. However, your previous professional experience counts. If you spent five years as a lead contractor before starting your own business, lenders view that as a sign of stability and reduced risk. You can learn more about specific strategies in our guide on how to get finance with a new ABN in Australia. The key is to demonstrate that while the ABN is new, your expertise is well-established and your business is a natural extension of that career.

Essential Documents for a Smooth Approval

While the process is streamlined, you still need to prove your business is viable. Being organised with your paperwork can lead to a much faster approval, sometimes within 24 to 48 hours. Most specialist lenders will require a basic set of documents to verify your identity and income potential. These typically include:

- Proof of Identity: A valid Australian driver's licence or passport.

- Active ABN: Confirmation that your business is currently registered and active.

- Bank Statements: Usually the most recent three to six months to verify cash flow and regular income.

- Contract of Works: Any signed agreements for future projects that prove your ability to service the loan.

Even if you have a thin credit file with very little borrowing history, having a clean record is a significant advantage. Lenders appreciate transparency. By showing a consistent history of on-time payments for smaller overheads, you build the trust necessary to secure larger asset finance for things like excavators or commercial mowers. Providing a "Contract of Works" is particularly powerful for landscapers, as it shows the lender exactly where the money to repay the loan will come from over the next six to twelve months.

Essential Landscaping Gear You Can Finance in 2026

Modern landscaping in Australia has evolved far beyond a trailer full of hand tools and a basic push mower. To compete for high-end residential projects or large scale maintenance contracts, you need a diverse fleet of specialised machinery. A landscaping equipment loan isn't just for your next work ute anymore. It covers the heavy hitters that perform the grunt work, allowing you to take on projects that were previously impossible for a sole trader to manage alone.

The Australian landscaping industry is projected to reach a value of USD 9.43 billion by 2034. This growth is driven by technology adoption and a shift toward more advanced design solutions. Whether you are clearing a block or maintaining a commercial parkland, having the right gear ensures you are part of this expanding market. Financing allows you to access this tech today rather than waiting years to save the necessary capital.

Major Machinery: Excavators and Bobcats

In rapid development zones like Melton or Hoppers Crossing, site clearing and preparation are the bread and butter of many local contractors. Buying a second-hand excavator or bobcat with cash might seem like a bargain upfront, but the risk of inheriting a "lemon" with hidden hydraulic issues can quickly derail your business. Financing new or near-new machinery ensures you have a manufacturer's warranty and the latest safety features. You can explore our specific Excavator & Bobcat Finance Options for Tradies to see how these heavy assets fit your monthly budget without compromising your cash reserves.

Commercial Mowing and Handheld Fleets

Maintenance masters know that speed is everything. High-end commercial zero-turn mowers are essential for large scale turf management, with prices for professional models often reflecting their high productivity. We are also seeing a significant shift toward battery-powered commercial fleets. These "green" transitions are becoming a competitive advantage as more local councils and premium clients demand low-noise and zero-emission services. You don't have to finance these tools one by one. You can bundle multiple smaller assets, such as motorised lawn care bundles which often cost around $8,699, into a single manageable landscaping equipment loan. This keeps your repayments predictable and your gear modern.

The Workhorse Category: Tippers and Trailers

Don't overlook the vehicles that move your business. Tipper trucks, specialised utes with custom toolboxes, and heavy-duty trailers are the backbone of any professional operation. A tipper truck can save you hours of manual shovelling every week, significantly reducing labour costs and physical strain. These assets are often the hardest working parts of your fleet and deserve the same financial consideration as your primary digging gear. If you are ready to expand your capabilities, apply for equipment finance today and get the gear you need to win bigger contracts.

How Quick Choice Streamlines Your Landscaping Loan

Finding the right landscaping equipment loan shouldn't feel like a second job. At Quick Choice, we act as your reliable specialist guide, taking the complexity out of asset finance so you can focus on your clients. Based in Truganina, we have deep roots in Melbourne’s West. We understand the specific demands of sole traders working in the booming estates of Tarneit and Werribee, where the ground is always moving and the work is constant.

We don't just offer one or two generic options. Our team does the heavy lifting by comparing products from a panel of over 40 different lenders. We look for the specific finance structure that aligns with your ABN and seasonal cash flow. Our streamlined approach follows a logical, three-step journey designed to save you time:

- Consultation: We discuss your business goals and the specific machinery you need to grow.

- Comparison: We scan the market to find the most competitive rates and flexible terms for your situation.

- Fast Approval: We manage the entire application process to get you a decision quickly, often within 24 to 48 hours.

Why a Broker Beats a Bank for Tradies

Traditional banks often use rigid "boxes" that don't account for the fluctuating nature of a landscaper's income. If your financial records aren't perfectly polished, a standard bank manager might struggle to see the potential in your business. We take a different view. We focus on your business story and your industry experience to find a lender that fits you. We handle the tedious paperwork and lender follow-ups so you can stay on the tools and on-site. For a comprehensive look at how we support independent contractors, read our Asset Finance for Self Employed: The Ultimate 2026 Australian Guide.

Ready to Level Up Your Landscaping Business?

Timing is everything in the landscaping trade. Securing your new excavator or zero-turn mower before the peak spring rush ensures you're ready to handle the surge in demand. We provide a professional, supportive service that values your time and your ambition. You'll work with a local partner who understands that your machinery is the heartbeat of your business. We take pride in helping Aussie sole traders move from basic maintenance to major project delivery through smart, bespoke finance solutions.

Don't let outdated gear hold your growth back. Contact the Quick Choice team for a bespoke quote today and get the machinery you need to take your business to the next level.

Build a Stronger Fleet for the Seasons Ahead

Growing a successful landscaping business requires more than just grit; it demands a strategic approach to acquiring the right machinery. By selecting a finance structure that protects your cash flow and utilising Low Doc options, you can secure the gear you need without the stress of traditional bank applications. A tailored landscaping equipment loan allows you to upgrade your capabilities today while keeping your working capital intact for future growth.

As specialist ABN and sole trader finance experts, we provide dedicated support to contractors throughout Western Melbourne. We take the hassle out of the process by providing access to over 40 Australian lenders, ensuring you find a solution that fits your specific trade requirements. You don't have to navigate the complexities of asset finance alone when you have a local partner who understands your market.

Organise your landscaping equipment finance with Quick Choice today and take the first step toward winning bigger contracts with modern, reliable machinery. We look forward to helping you take your business to the next level.

Frequently Asked Questions

Can I get a landscaping equipment loan with a new ABN?

Yes, you can secure a landscaping equipment loan with a new ABN, though your choice of lenders might be narrower than an established business. Specialist lenders often value your previous industry experience and future contract work more than the age of your ABN. We focus on helping you present a strong business case to secure the gear you need to get your new venture off the ground.

What is the minimum ABN trading period for a low doc equipment loan?

Lenders typically look for a minimum of 12 months of active ABN trading for a standard Low Doc loan. However, some specialist providers will consider applications from sole traders who have been in business for as little as six months if they have relevant industry history. Having a clean credit file and an active GST registration will significantly strengthen your application in these scenarios.

Do I need to provide my house as security for a machinery loan?

No, you don't need to use your family home as security for a machinery loan. These are asset-backed loans, which means the mower, excavator, or truck you are buying acts as the collateral for the debt. This structure is ideal for sole traders who want to keep their business and personal assets separate while still accessing competitive interest rates for their fleet.

Are landscaping equipment loan repayments tax-deductible?

Repayments for a landscaping equipment loan are generally tax-deductible, but the specific method depends on your finance structure. With a chattel mortgage, you can typically claim the interest component of the repayments and the asset's depreciation. If you choose a finance lease, the monthly lease payments are usually fully deductible as a business expense, making it a simple option for tax time.

Can I finance used landscaping equipment or only new gear?

You can certainly finance used landscaping equipment, provided it meets the lender's age and condition standards. Most finance providers prefer the machinery to be no older than 10 or 12 years at the end of the loan term. This flexibility allows you to pick up quality second-hand gear that still has plenty of life left, saving you money on the initial purchase price.

How long does the approval process take for an equipment loan?

Approvals can be secured in as little as 24 to 48 hours when you work with a specialist broker. Because we understand the documentation lenders require, we can package your application correctly the first time. This speed is vital when you need to replace a broken machine mid-season or want to take advantage of a limited-time sale at a dealership.

What is a balloon payment and should I use one for my mower loan?

A balloon payment is a pre-determined lump sum that you pay at the end of your loan term. By deferring a portion of the principal, you lower your monthly repayments, which is a great way to manage cash flow during quieter months. At the end of the term, you can choose to pay the amount in full, sell the gear, or refinance the remaining balance.

Is GST included in the financing of landscaping machinery?

Yes, you can finance the GST-inclusive price of your machinery. If your business is registered for GST and you use a chattel mortgage structure, you can usually claim that GST component back as an input tax credit on your next Business Activity Statement. This provides a significant cash flow injection back into your business shortly after you've put the new equipment to work.